For years, DeFi lived and breathed around one simple idea: lock capital, lend it out, and earn yield. Trading existed, but mostly as a secondary layer. By 2025, that hierarchy has flipped on its head. Lending is losing momentum, yield farming has thinned out, and Perp DEXs are steadily absorbing revenue, liquidity, and attention across the entire ecosystem.

This is not a temporary rotation driven by hype. It reflects a deeper structural shift in how yield is created and how capital actually works on-chain.

When Lending Stops Being the Center of the Value Chain

The problem with DeFi lending was never poor design. It was structural. Most lending protocols rely on heavy overcollateralization. To borrow one dollar, users typically have to post $1.30 to $1.50 in assets. This keeps the system robust, but it also locks up enormous amounts of capital that generate relatively little economic activity.

As a result, capital velocity remains low. The majority of users deposit assets not to actively trade, but to park funds and earn passive interest. Protocol revenue therefore scales almost entirely with TVL and borrowing demand. Growth becomes linear: to earn more, the system needs proportionally more capital.

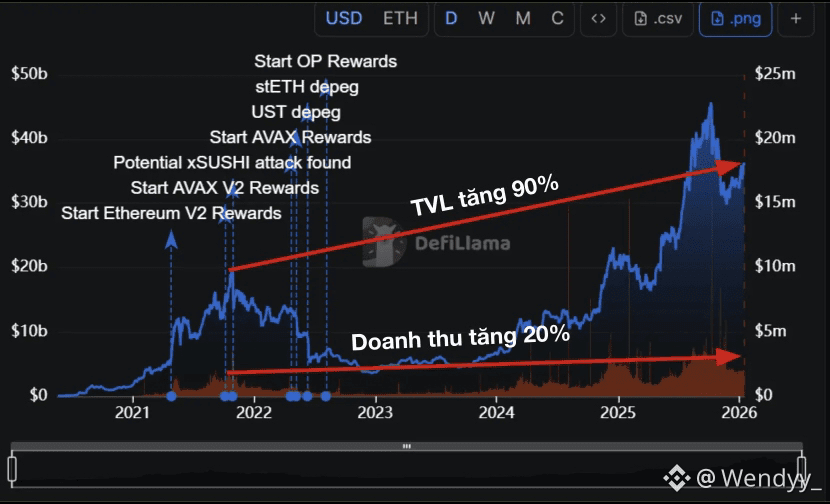

That limitation is becoming more visible as DeFi matures. Even though Aave, the largest lending platform, has seen its TVL recover strongly compared to the 2022 peak, protocol fees have grown far more slowly. Yield per unit of capital has compressed, revealing a declining efficiency curve.

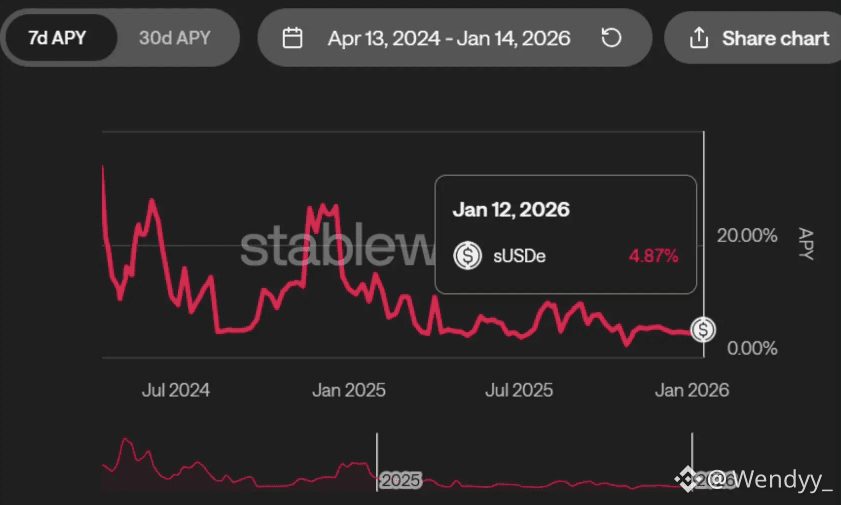

Bull markets only amplify this weakness. When asset prices rise quickly, borrowing demand often falls. Traders no longer need leverage to feel exposure, and many unwind leverage loops altogether. Stablecoin APYs drop, sometimes toward levels that feel indistinguishable from TradFi. Lending gradually shifts from a yield engine into a low-risk liquidity warehouse — safe, but increasingly uncompetitive in an active market.

As soon as stablecoin yields hover near single digits, capital behavior changes. Funds stop tolerating inactivity. They migrate toward areas with higher turnover, greater volatility, and clearer paths to amplified returns. This migration erodes lending’s role as the core economic layer of DeFi and creates space for trading-driven models to move center stage.

Why Perp DEXs Win on Capital Velocity

Perp DEXs are built on an entirely different philosophy. Instead of immobilizing capital for safety, they aim to maximize how often that capital is used. Through leverage, a relatively small base of collateral can support enormous notional trading volume.

A trader with $10,000 can open a $200,000 position using 20x leverage. Fees are charged on the full notional size, not the underlying collateral. This creates something lending cannot replicate: revenue leverage. The same dollar can be “reused” many times in a single day to generate fees.

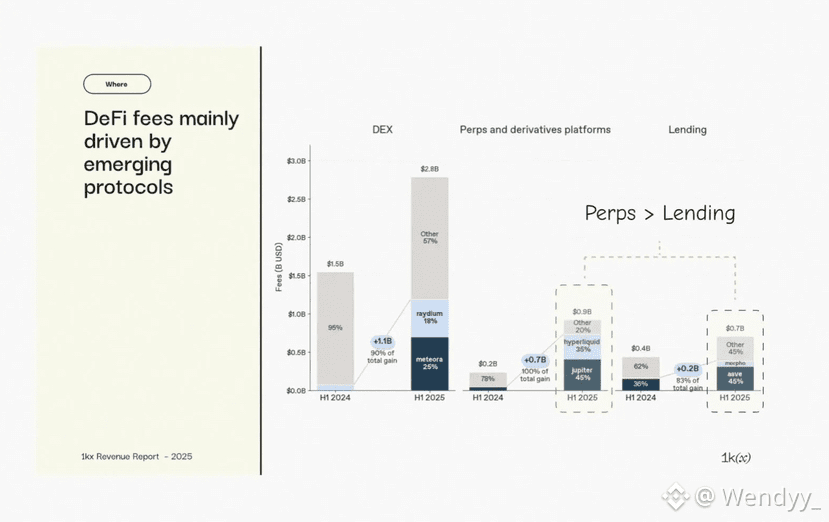

The revenue data reflects this shift clearly. In 2024, on-chain derivatives generated far less in fees than lending. By 2025, Perp DEX fees have surged dramatically, outpacing lending not because more capital is locked, but because capital is moving faster. Volatility, once a risk factor, becomes a direct input to revenue.

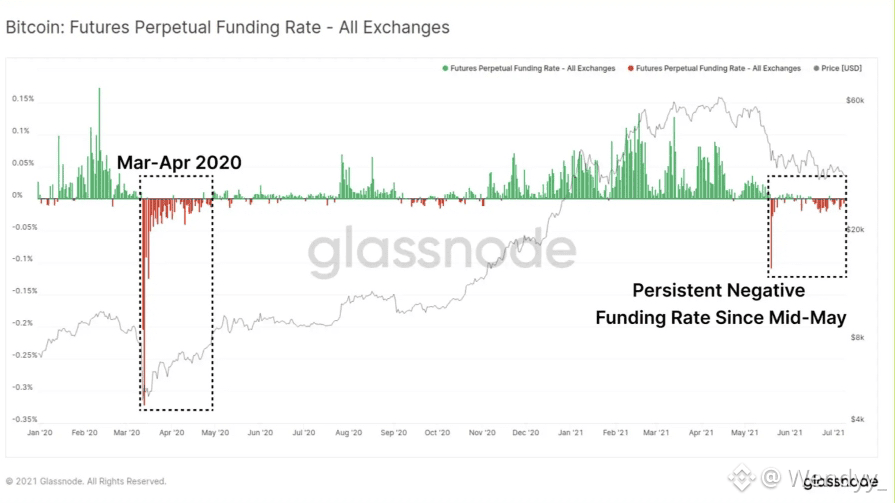

Funding rates illustrate this perfectly. During periods of extreme market imbalance, funding swings sharply as longs or shorts dominate. These phases consistently coincide with spikes in trading volume and liquidations, which translate directly into protocol income. Where lending must defend itself during turbulence, Perp DEXs monetize it.

Lending protocols do not possess a comparable volatility-to-revenue conversion mechanism. In stressed markets, their priority is risk containment: liquidations, parameter adjustments, and loss prevention. Interest rates may rise, but rarely fast enough to offset the systemic risk. For lending, volatility is a threat. For Perp DEXs, it is fuel.

If lending resembles a credit system that thrives on stability, Perp DEXs function as financial infrastructure designed to harvest speculation and hedging demand in real time.

A New Yield Stack Built Around Perp DEXs

Once Perp DEXs became the dominant source of real on-chain cash flow, a new yield ecosystem began forming around them. Instead of manufacturing yield through emissions or relying on inefficient lending spreads, protocols increasingly anchor returns directly to derivatives activity.

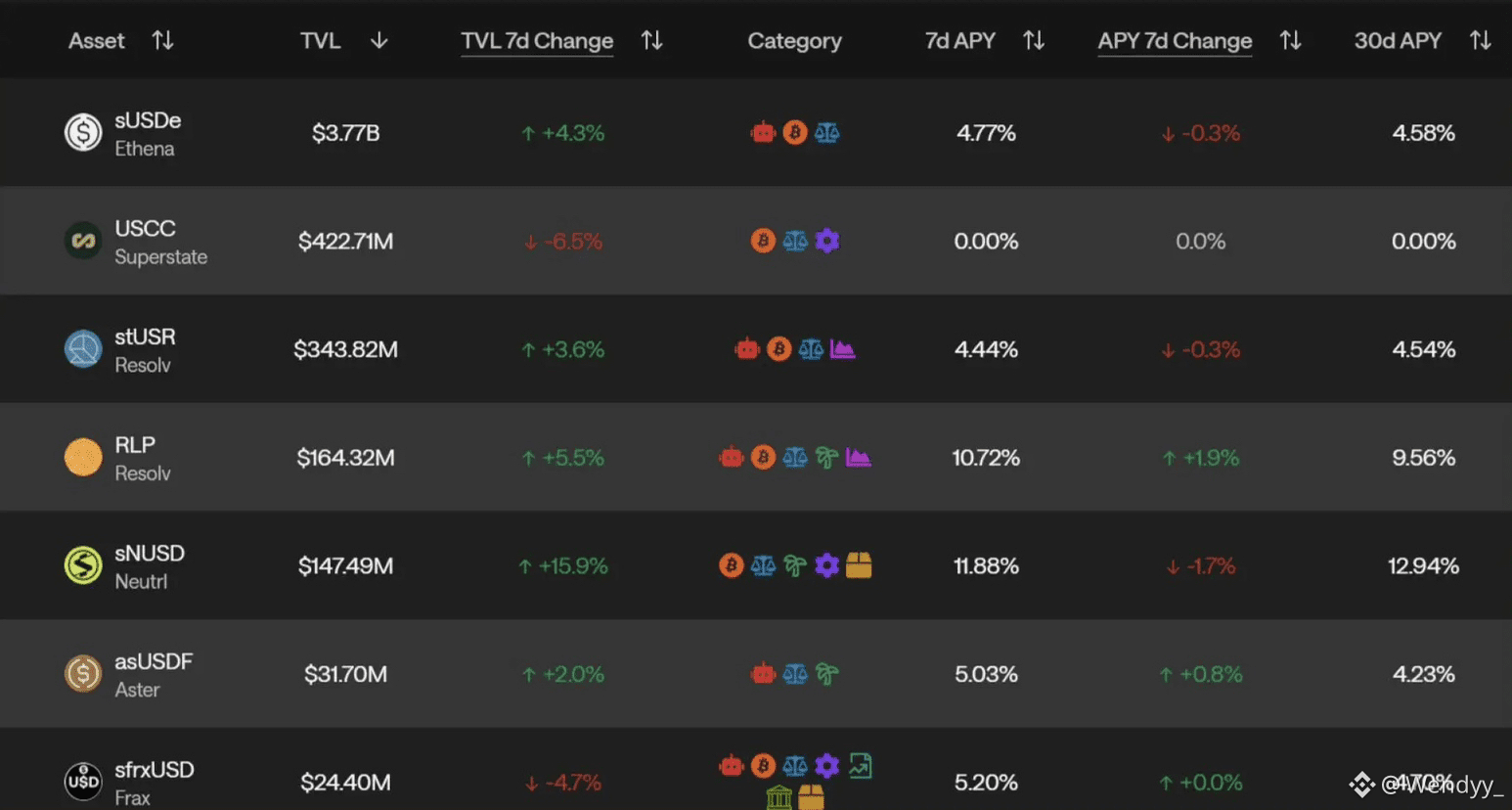

Vaults like HLP on Hyperliquid allow users to deposit USDC and act as counterparties to traders, earning fees and benefiting from trader losses. GLP on GMX captures trading fees and liquidation value. Ethena’s USDe extracts funding rates through delta-neutral positioning, transforming leverage demand into stablecoin yield.

At the monetary layer, yield no longer comes from borrowers paying interest. It is pulled from funding rates, liquidations, and trading fees. Stablecoins evolve from passive settlement assets into yield-bearing instruments tied directly to perpetual markets. Volatility, once something to hedge away, becomes the underlying source of income.

In yield markets and structured products, protocols like Pendle integrate perp-linked returns, enabling future yield streams to be separated, priced, and traded. Yield stops being a side effect of locked capital and becomes a financial primitive in its own right.

At the strategy and vault layer, Perp DEXs increasingly serve as the default execution venue. Market making, basis trades, and risk-neutral strategies all feed on deep liquidity and constant trading flow. These systems do not compete with Perp DEXs; they parasitize their activity, packaging derivative-driven yield for different risk profiles.

Over time, this reorients DeFi’s architecture. Perp DEXs sit at the center, generating raw cash flows. Surrounding protocols focus on structuring, distributing, and optimizing those flows. Lending does not disappear, but it shifts to the periphery, supporting liquidity rather than defining yield.

The quiet truth is that DeFi is no longer organized around locked capital. It is organized around capital in motion. And Perp DEXs, by design, are where that motion never stops.

This article is for informational purposes only. The information provided is not investment advice