When people think of crypto, the first two names that usually pop up are Bitcoin and Ethereum. For a lot of folks, the third is $XRP .

For me, the third crypto is actually Solana but we’re not talking about that today.

A friend recently told me to seriously look into XRP. I did. And after digging through the numbers, the legal history, and the real-world adoption, I personally decided to add it to my portfolio and keep stacking.

In this article, I’ll break down the moral debate, the financial case, and the real facts behind XRP.

Let’s get into it.

The legal battle that changed everything

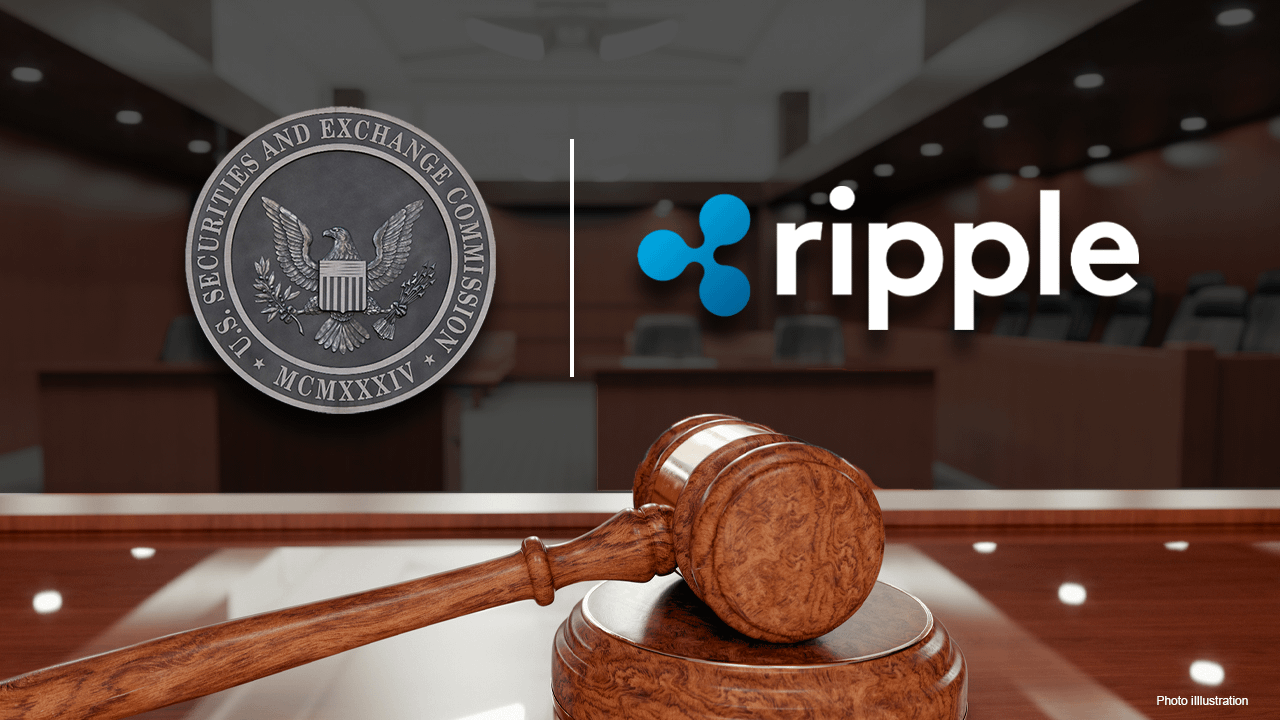

Before anyone talks about XRP as an investment, the SEC lawsuit has to be addressed.

In December 2020, the SEC sued Ripple Labs, claiming XRP was sold as an unregistered security. XRP got crushed, delisted from major U.S. exchanges, and basically became “toxic” in the U.S. market.

Then came the turning point.

In July 2023, Judge Analisa Torres ruled:

Retail XRP sales on exchanges were not securities

Institutional sales were treated differently

Ripple paid $125M, far less than the $2B the SEC demanded

By 2025, the SEC backed off. Appeals were dropped, money was returned, and by August 2025 the case was officially done.

This matters more than most people realize. XRP went from being at risk of getting wiped out in the U.S. to having regulatory clarity almost no other crypto has.

What XRP actually does

XRP isn’t trying to replace Bitcoin or compete with Ethereum.

Its focus is simple: cross-border payments.

The current system is outdated. International transfers can take 2 to 5 days, cost heavy fees, and move through multiple banks. It’s slow, expensive, and inefficient.

XRPL solves this by settling transactions in seconds with near-zero fees.

The real breakthrough is On-Demand Liquidity:

Convert local currency into XRP instantly

Send XRP in seconds

Convert into the destination currency immediately

No need to pre-fund foreign accounts

No capital locked up

This is the difference between moving money like the 1970s and moving money like the internet.

Who’s actually using it

What convinced me to take XRP seriously is adoption.

This isn’t just another crypto with a “future roadmap.” Institutions are already integrating Ripple’s tech. Japan’s SBI has been one of the biggest supporters, and Ripple’s payment network is active across dozens of markets.

These aren’t just pilots. This is real payment infrastructure being used in production.

The financial case and why I’m stacking

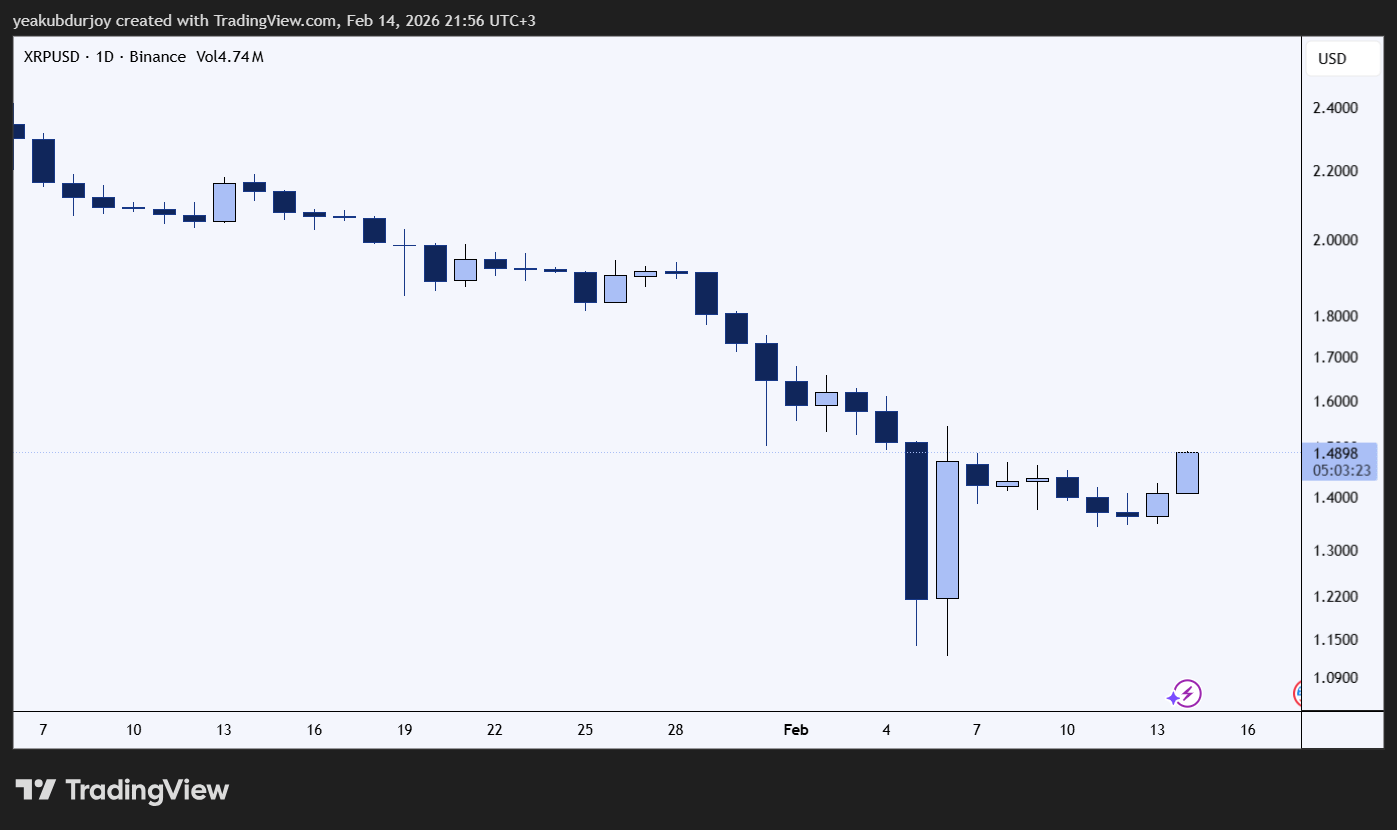

XRP is currently sitting around the 1.5 range and still ranks as one of the biggest cryptocurrencies in the market.

What changed my mind:

Legal clarity: XRP fought the SEC and survived

Real adoption: banks are actually using Ripple’s rails

Massive market size: SWIFT moves trillions daily

Institutional access: futures and ETF narratives are building

Risk/reward: clearer than most altcoins

Could XRP drop hard? Yes. If the macro environment turns ugly, it can fall back to lower.

But compared to most projects, XRP has something rare: a clear use case, real adoption, and legal clarity.

The moral debate

Yes, XRP is more centralized than many people like. Ripple created the supply upfront and still holds influence.

But honestly, that may be the reason banks are willing to work with it.

If your goal is pure decentralization and anti-bank ideology, XRP probably isn’t your play.

If your goal is owning a crypto asset that institutions can realistically adopt, XRP makes sense.

My strategy

I added XRP at around a 5% to 10% portfolio allocation.

Not an all-in bet. But enough exposure that if this plays out, it matters.

My plan is simple:

DCA over the next 2 to 3 months

Hold for at least 1 to 2 years

Accept volatility

Take profits in stages

What could go wrong:

A new bear market

Banks use Ripple tech without using XRP

Regulations shift again

Competition from CBDCs and other settlement systems

Still, after weighing everything, the setup looks stronger than most crypto narratives.

The bottom line

The real story behind XRP is this:

It was built for global payments. It got crushed by the SEC. It survived. Now it has a level of regulatory clarity and institutional traction that most crypto projects can only dream about.

It’s not trying to be Bitcoin or Ethereum. It’s solving a massive problem, making international transfers faster and cheaper.

Is it guaranteed to pump? No.

Can it still drop 50%? Absolutely.

But after looking at the facts, the adoption, and the market opportunity, I’m confident enough to keep stacking.

Not financial advice. Always do your own research.

And for full transparency, AI was used during drafting mainly for source referencing and writing improvements.

Anyway, wish everyone a great day.

Good luck.