Key metrics: (17Nov 4pm HK -> 1Dec 4pm HK)

BTC/USD -9.6% ($95,600-> $86,400), ETH/USD -11.9% ($3,200 -> $2,820)

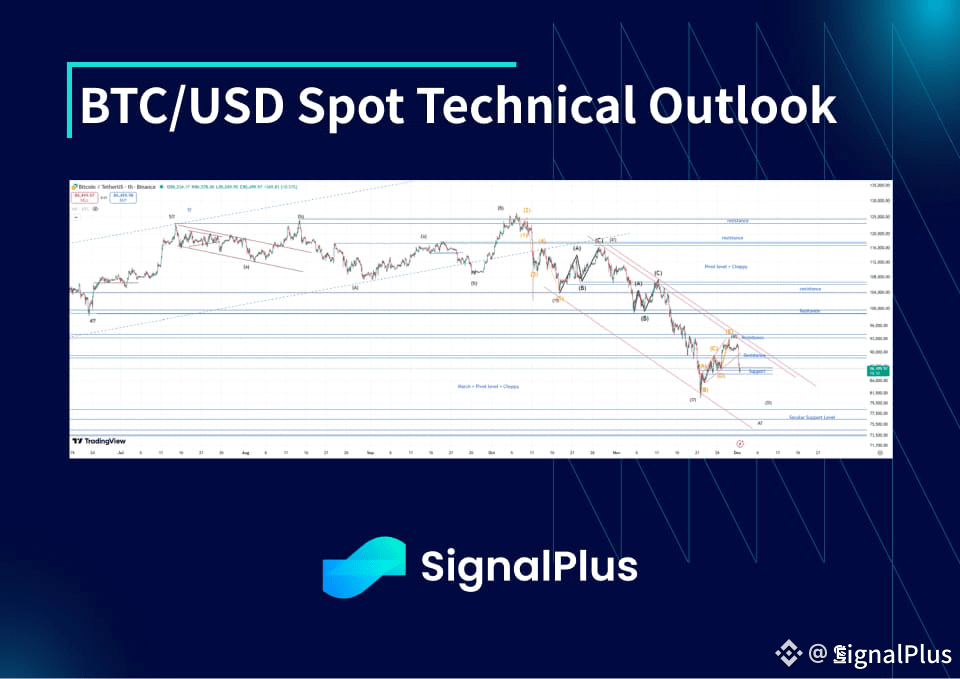

After a plunge down towards key support at $80k two Fridays ago, last week was categorised as a corrective climb back from the lows as the market in thin Thanksgiving liquidity attempted to regain a solid footing ahead of an anticipated “Santa” rally. This week began with a reality check: the overhang of longs still out there, and the pivot level of $89k triggered some heavy selling over the Asian session. While we do expect the market to engineer a ‘Santa rally’ later in the month (especially in light of Fed expected to cut rates), we initially (continue) to expect that the most likely path forward is a re-testing of the lows from here, but that low will be a longer term buying opportunity. Participants that didn’t sell the bounce-back last week might be panicking a little, especially if we don’t see a quick recovery/climb back towards the resistance lvls ($88.5–90k) and that would catalyse the move lower

There are a few alternative “counts” and possible price paths out there — more so than usual owing to the complications of the Oct flash crash — so there is a non-trivial probability that this is simply a correction of an overshoot higher on thin liqudiity and that the longer term move higher is already in play. A final alternative is this is still part of the corrective move before the last leg lower (this will be evident if we reclaim > $90k but fail at $100k) but odds are on more downside price action from here this week. We suggest scaling into longer term longs from here ($85.5–86.5k lvl) and again closer to $80–81k and for the daring, more $78–80k (big secular support comes in below that). Key pivots to the top side include > $89k and through $94.25k, with $100k the key pivot to open us back up to $125–130k region (our target for wave B, which comes after this move is done)

Market Themes

Volatile couple of weeks across markets as the FOMC pricing pendulum swung from 90% odd of a December cut down to 30% and back up to 90%. High-beta tech/AI names and crypto suffered the most, while VIX briefly re-visited the local highs of 25–26 that we have seen on a few occasions this year (excluding the March-April tariff highs >40), though once again this level capped pricing as the fundamental macro backdrop remains broadly risk supportive in the absence of any material change to the Fed’s rate path. The market’s capacity to sustain risk-off for an extended period of time remains limited as positioning lightened up into Thanksgiving and we saw a broad relief in risk assets

After leading the move down in the high-beta risk complex, crypto was not spared from an extension of the move lower, with BTC cracking key support at $85k and triggering a fast move down to test strong support at $80k two Fridays ago. From there we have seen a corrective bounce in thin liquidity and selling exhaustion set in and broad risk sentiment bounced, with the market attempting to call the bottom. Unfortunately it seems that sentiment/market structure has been fundamentally weakened following the events of 10th-11th October and so this cycle ‘might be different’ in the sense that buying appetite and fresh liquidity may not be plentiful enough to drive a material surge back through $100k. IBIT outflows have picked up but nothing near the extent of the months of continuous inflows we saw since the summer and the trend of flows there will be key to monitor going forward. Interestingly alt coins have held up relatively better which is very unusual for ‘bear markets’ in crypto, which is suggestive of much deeper de-leveraging (again related to the effects of 10th-11th October) and with alt coin positioning broadly much cleaner (outside of the DAT holdings, though Tom Lee shows no signs of slowing purchases of ETH… yet!)

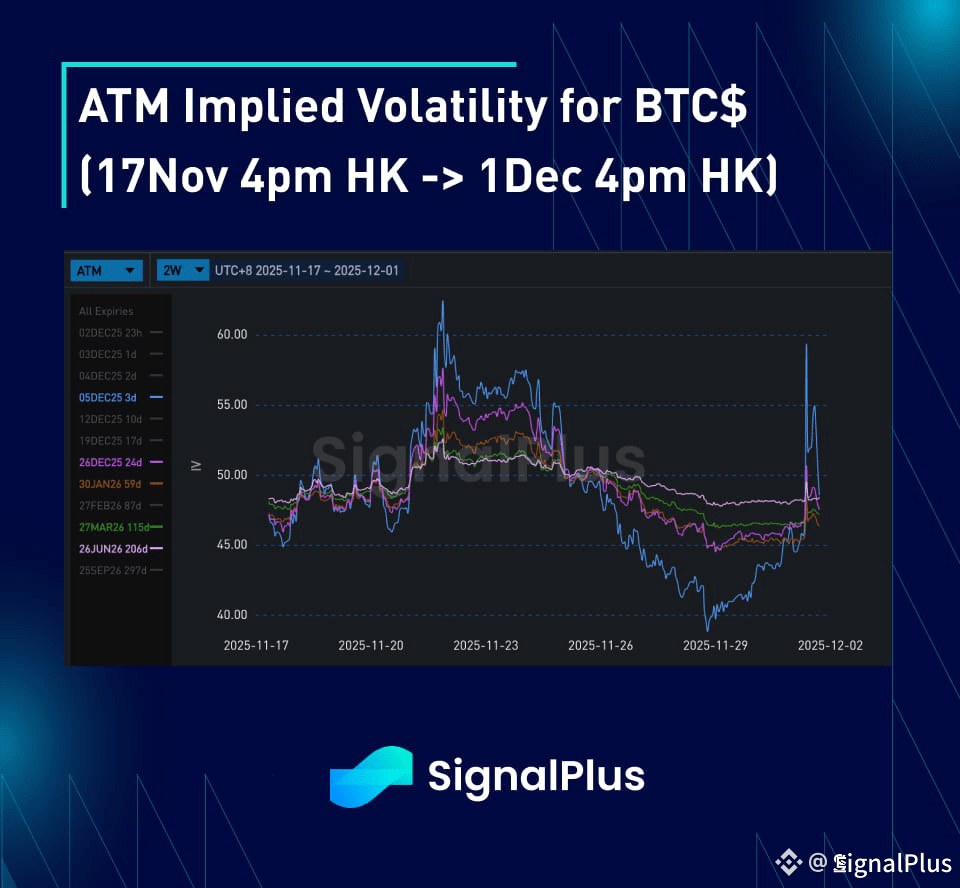

BTC$ ATM implied vols

Implied vols exhibited a big range in the past 2 weeks as <2m contracts exploded higher as spot tested down to $80k before having a sharp sell-off last week as spot exhibited a low realised corrective grind higher, before picking up again with the fresh sell-off from $90.5–85.5k in Asia. Realised performance has actually remained healthy in the high 40s/low 50s, so the sell-off in implied vols can only be attributed to position reduction into year end, with dealers looking to recycle any selling flows from unwinds of directional plays.

The term structure of implied vols has flattened up broadly as some supply of back-end vols has left >3m expiries a little heavy, while front-dated contracts remain supported due to elevated realised

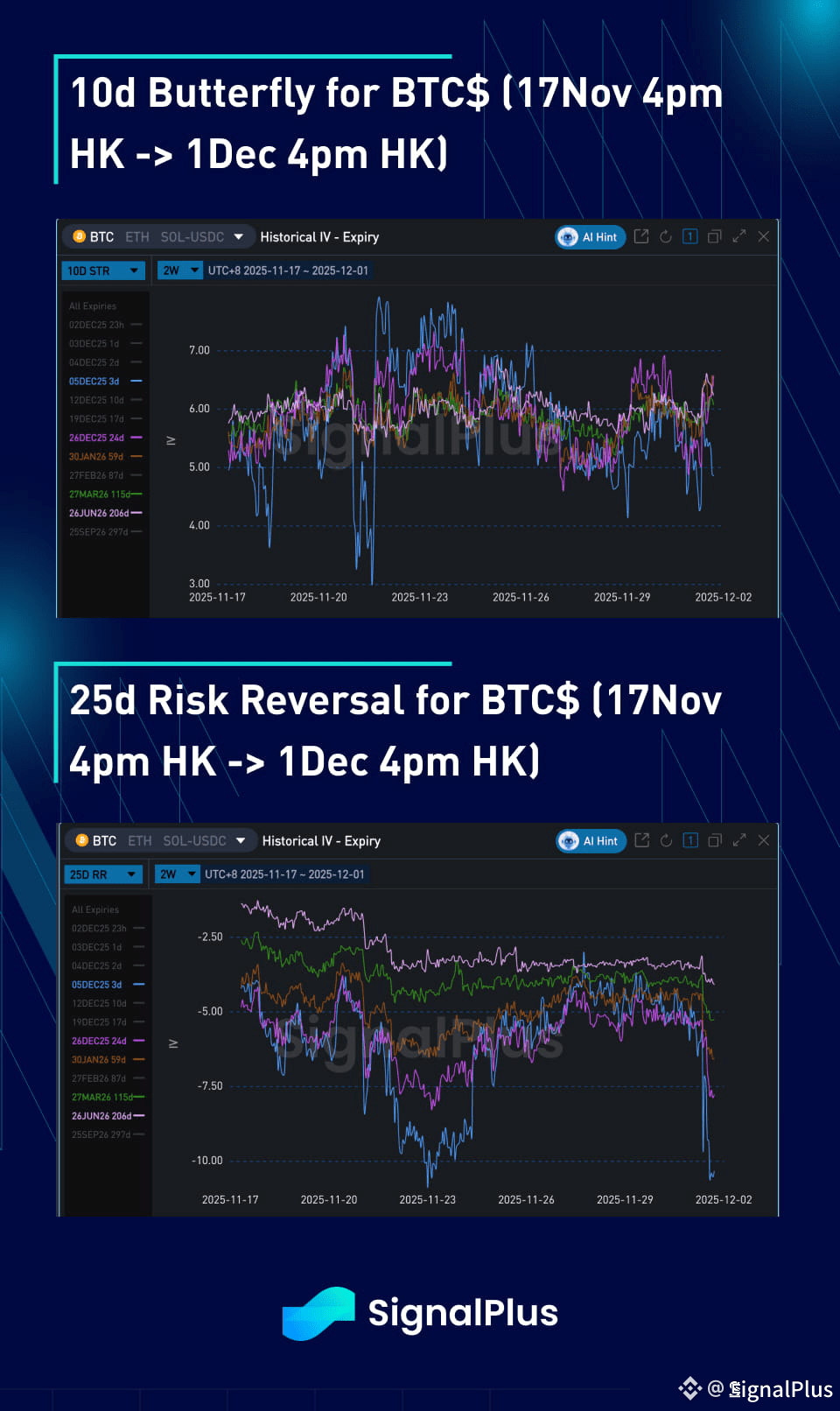

BTC$ Skew/Convexity

Skew prices have broadly been tracking the directionality of spot, and the realised spot-vol correlational (both realised and implied vol) has been incredibly strong. From a supply-demand dynamic the market has started to see overlay supply of calls again even at these spot levels and this should continue to keep skew prices bid deeply for puts

Convexity prices have been broadly sideways as spot finds a footing in the broad $80-94k range. Directional plays either side of this range have been in call-spread or put-spread format supplying more wings to the market, with limited expectation of a material break of this range anytime soon. Also with local gamma realising healthily this has also created more appetite for local strikes over wings

Good luck for the week ahead!