The majority of blockchain accounts start with the philosophical concept of decentralization. The initial hype was ideological: eliminate the middle men, open everything up, and have transparency take the place of the trust. In the case of Dusk Network, decentralization is not an ideology, but a very real need of the next phase of finance. Financial regimes do not collapse due to the presence of intermediaries, instead, they collapse due to the abuse of information, perverse incentives or a collapse of trust in stress. That institutional reality is the beginning of Dusk. It is not aimed to replace banks, but to offer the infrastructure which can be utilized by regulated finance in the real-life without abdicating the fundamental advantage of blockchain: programmability, verifiability and self-custody.

Dusk is a privacy-focused chain, in contrast to general-purpose chains, which views privacy as an option or an external concern. This distinction matters. Transparency does not meet hostility in institutional markets - the exposure to them is hostile. According to the conventional finance transparency is limited to certain checkpoints: audits, reporting, supervision. It lacks as a stream of public performance of all internal actions. Dusk operates under the same reasoning on-chain with confidentiality being the default state but allowing the ability to demonstrate correctness when needed.

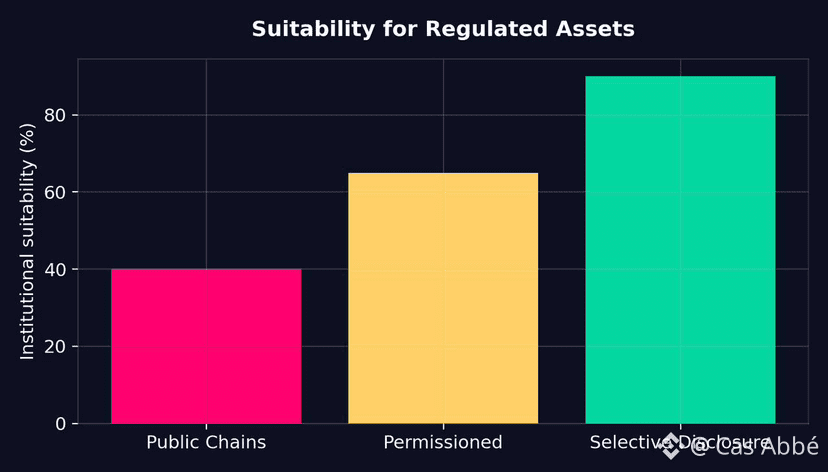

Visibilities that are not controlled are not supported by regulated markets since visibility itself becomes a market risk. Institutional liquidity pools of tokenized real-world assets, regulated securities, or other tokenized assets cannot work when all the trades, counterparty interactions, or strategic allocations become public metadata. Transaction graphs are leaky even in the absence of identities. Timing reveals strategy. Size reveals conviction. Flow reveals positioning. The monetization of such information is attainable in the real markets. The solution that Dusk offers to this issue is the privacy-preserving smart contracts and zero-knowledge cryptography, which enable a transaction to be performed confidentially and yet produce provable evidence of compliance.

There is a regulatory fact that is of little essence but much importance in this design. It is not that regulators are striving to observe everything, they are just trying to make sure that rules are enforced. Their concern is provability, but not voyeurism. The coming of dusk concedes this and leads to it so that a selective disclosure is possible, as opposed to full disclosure. It does not make institutions decide between the open and closed systems but provides them with the third option: the public infrastructure with restricted visibility.

The question as to whether this vision can scale depends on architecture. Dusk is developing a multilayer stack decoupling consensus, settlement and execution issues. This division is non-cosmetic. It permits privacy assurances to be implemented on the execution level and settlement checked as well as consensus on the consensus made. To institutions, this minimizes the integration risk. Systems are able to have an interface into the layer which they require without providing unwarranted exposure on others.

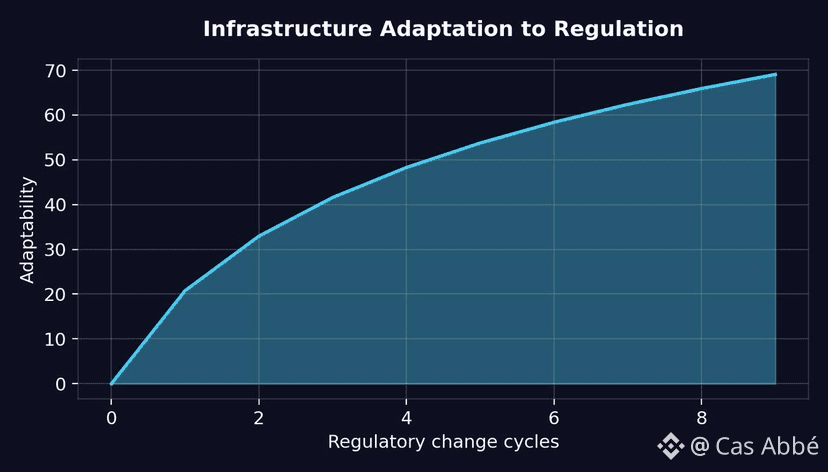

The concept of modularity is also important since compliance structures do not remain the same. Regulation regimes, such as MiCA, EC-DLT and national securities regulations, are developed by amendment, interpretation and enforcement practice. Infrastructure that is not adaptable enough to maintain compatibility is no longer useful. The modular upgrade paths at Dusk are meant to accommodate change in regulations without necessarily compelling the markets to stop, to migrate or to rewrite their assumptions. It is the way of real financial infrastructure maintenance.

There are practical implications of such design choices. The adoption of Chainlink and its data standards and interoperability protocols, as well as its partnership with regulated venues, such as the Dutch exchange NPEX, is an indication that Dusk focuses on institutional processes and not speculative volume. The integrations concern data integrity, controlled price feeds, compatible settlement, and interoperability with the already existing market infrastructure. That is, they seek to make Dusk practical where legal responsibility and operational fidelity are concerned.

Finally, technology does not make success. Adoption does. And in controlled settings the adoption is maintained on another schedule. It goes through pilots, regulatory reviews, internal risk assessments, and progressive scaling. This does not amount to friction, but the price of legitimacy. In the case with Dusk daily users are not the relevant metric and spikes of activity are not relevant as well. Whether the issuers and custodians, exchanges and settlement agents commence to route real issuance and post-trade flows its rails or not.

In case privacy and compliance are put on the same level as a prerequisite to institutional engagement - as the present tendencies indicate that they will be - the positioning of Dusk will agree with this future. This question is whether institutions will integrate this infrastructure so that it builds structural retention. Such a solution will not come soon, but will make or break Dusk to optional tooling or essential plumbing within the next 10 years.