The biggest misconception about payments is that cost lives where the swipe happens. Consumers see “₹0 fee,” “0% surcharge,” or “free transfer,” and assume the system is efficient. It isn’t. The cost of moving money rarely shows up at checkout it shows up in the settlement layer, the reconciliation layer, and the treasury layer that merchants quietly fund without ever itemizing it on a receipt.

The biggest misconception about payments is that cost lives where the swipe happens. Consumers see “₹0 fee,” “0% surcharge,” or “free transfer,” and assume the system is efficient. It isn’t. The cost of moving money rarely shows up at checkout it shows up in the settlement layer, the reconciliation layer, and the treasury layer that merchants quietly fund without ever itemizing it on a receipt.

That buried cost is why payment infrastructure changes slowly. It isn’t the UX that breaks first it’s the unit economics behind the scenes. And this is exactly the part of the stack Plasma is targeting with clinical focus: the invisible friction that merchants absorb long after the consumer thinks their transaction is “done.”

Checkout Ends When Settlement Begins

If you’ve ever managed merchant operations, you know the checkout moment isn’t the financial event it’s the theatrical performance. The payment terminal beeps, the app flashes green, the customer walks away. What happens next is the part that decides whether margins survive.

Funds batch, clear, reconcile, settle, get bridged across issuers, card networks, acquirers, PSPs, banks, and treasury accounts. Sometimes D+1, sometimes D+3, sometimes longer if cross-border corridors or compliance checks intervene. During that lag, merchants are effectively extending credit to the system.

Consumers call it convenience. Merchants call it float.

Crypto promised to fix this. Stablecoins actually could but not on chains designed for speculation rather than settlement. Fast block times don’t matter if the finality model is probabilistic. Low gas doesn’t matter if fees spike under load. User UI doesn’t matter if treasury doesn’t trust the ledger.

Plasma’s bet is brutally simple: the winning chain won’t be the one that feels good to send on it’ll be the one that feels reliable to settle on.

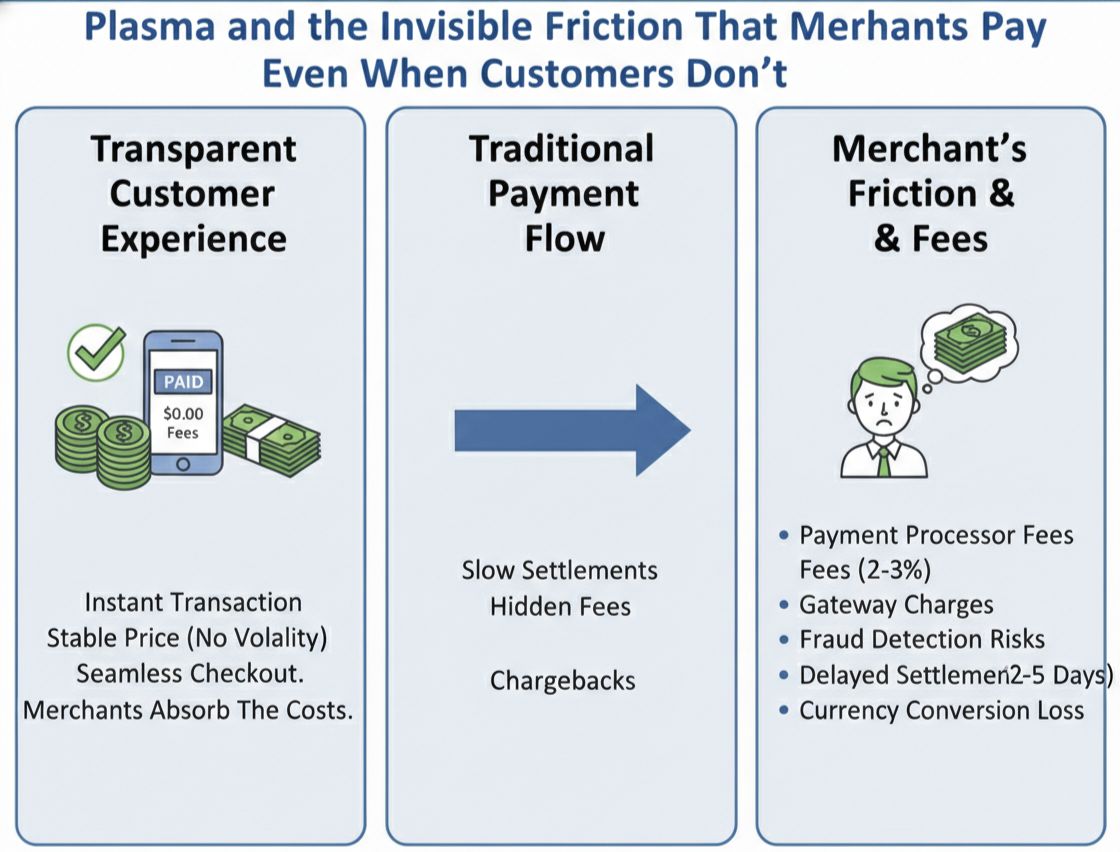

The Hidden Costs That Make “Free Payments” Expensive

Stablecoins already removed volatility from transfers, but they didn’t remove the four underlying merchant burdens:

01. Settlement Uncertainty

A transfer pending is not a transfer settled. Merchants need deterministic finality, not “usually final after N confirmations.” PlasmaBFT gives sub-second finality that behaves like a guarantee, not like a loose probability curve.

02. Reconciliation Overhead

Treasury teams don’t care that the transfer was fast they care whether the ledger matches the books. If reconciliation requires retries, retries become overhead, overhead becomes cost, and cost becomes margin compression. Plasma reduces reconciliation drag by making transfers idempotent and predictable.

03. Float Financing

Every delay between booking and settlement is a short-term financing event merchants subsidize without ever itemizing it. A chain that settles stablecoins instantly compresses float into near-zero.

04. Gas Friction

The most absurd cost in crypto is forcing a merchant to hold a volatile token to spend a stable token. Plasma eliminates this with stablecoin-first gas mechanics and gasless USDT flows.

None of these costs appear on a customer receipt. All of them appear on the P&L.

Why Stablecoins Need a Settlement Chain, Not a Trading Chain

Stablecoins succeeded faster than any blockchain infrastructure designed to support them. They rode trading rails, not payment rails. That created an odd mismatch:

stablecoins evolved into money

but they’re still settling through markets

Markets tolerate latency and probabilistic finality because traders hedge against variance. Merchants don’t. Merchants need the equivalent of ACH, FPS, UPI, and card settlement but programmable, global, and censorship-resistant.

Plasma re-architects the stack around this reality:

✔ stablecoin-centric execution

✔ deterministic sub-second finality

✔ Bitcoin-anchored immutability

✔ EVM environment for composability

✔ no native-token tax on payments

✔ treasury-friendly ledger behavior

This isn’t a chain competing for DeFi bragging rights it’s a chain trying to win the boring parts of money movement that decide whether stablecoins become infrastructure instead of trading tools.

The Merchant Mindset is Where Real Adoption Hides

Consumers adopt based on UX.

Merchants adopt based on unit economics.

Treasury adopts based on reconciliation risk.

Institutions adopt based on settlement guarantees.

Plasma is building for the last three.

Plasma is building for the last three.

Most chains never get there because they optimize for what looks impressive on a dashboard: TPS demos, throughput numbers, 3D block explorers, and performance theater. Plasma optimizes for conditions that never trend on Twitter: predictable settlement, reconciliation stability, float compression, and zero-gas friction.

That’s why the phrase “invisible friction” matters the frictions that matter most are not visible to users, they are visible to accountants.

The Punchline: Stablecoins Don’t Win Until Merchants Win

Stablecoins already work for traders.

They work for remitters.

They work for cross-border freelancers.

But they haven’t “won” payments because they haven’t reduced the merchant burden enough to displace existing rails.

Plasma’s argument is that the moment you compress settlement friction to zero and treasury risk to negligible, stablecoins stop behaving like crypto and start behaving like money.

At that point adoption doesn’t accelerate it compounds.

And compounding adoption always starts with merchant economics, not consumer hype.