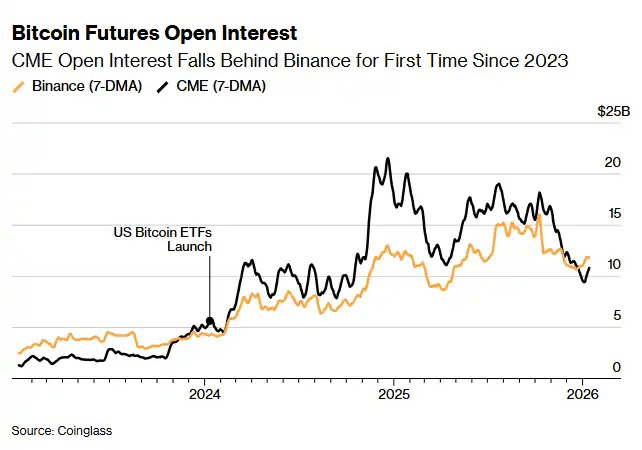

The cryptocurrency derivatives market is undergoing an unprecedented structural transformation. Bitcoin Cash and arbitrage trading, once regarded by Wall Street institutions as a 'risk-free money printer', have now completely lost their luster, with arbitrage opportunities compressed to levels rarely seen in recent years; the open interest in Bitcoin futures on the Chicago Mercantile Exchange (CME) has been surpassed by Binance for the first time since 2023. This landmark change not only signals the end of the risk-free high-yield era in the crypto market but also releases a core signal of the market's transition from wild growth to maturity and diversification.

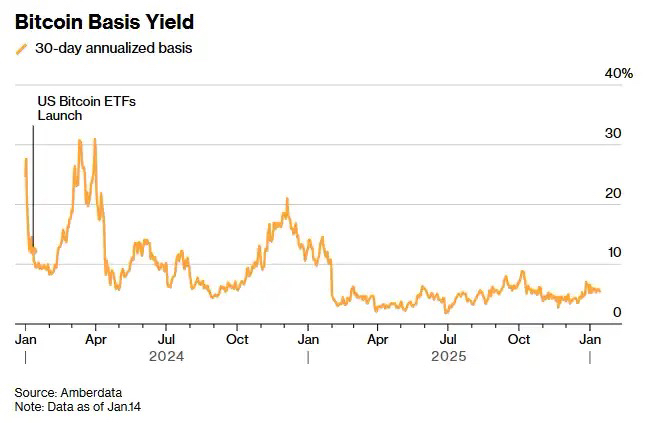

The starting point of this transformation is the launch of the spot Bitcoin ETF in early 2024. At that time, the ETF opened the compliant door of the crypto market to traditional institutions. CME, with its compliance and standardized contracts, became the preferred venue for Wall Street to conduct cash and arbitrage trading. This strategy, which is highly similar to traditional market basis trading, achieved double-digit annualized returns by buying spot Bitcoin through the ETF while simultaneously selling CME futures to profit from price differences. This attracted billions of dollars in arbitrage funds, making Delta-neutral strategies the hottest trading choice at that time. However, the rise and fall of the ETF led to a situation where as more trading desks entered the market to share the dividends, the arbitrage price difference was quickly erased, and the script of this wealth creation game was destined to be rewritten.

According to the latest data from Amberdata, the annualized yield of cash and arbitrage trading for Bitcoin with a one-month term is only around 5%, while a year ago, the basis for this strategy was close to 17%. It has now dropped to 4.7%, barely covering the cost of funds and execution. Compared to the 3.5% yield on one-year U.S. Treasury bonds, this once-popular strategy has lost much of its appeal. Against the backdrop of declining profits, the open interest in CME Bitcoin futures has plummeted from a peak of $21 billion to below $10 billion, while Binance, which focuses on perpetual contracts, maintains a stable size of about $11 billion. The reversal of the exchange landscape has become the most intuitive reflection of changes in market structure.

It is worth noting that the shrinkage of CME's scale is not a comprehensive retreat from the crypto market but a 'tactical reset' of institutional funds. James Harris, CEO of Tesseract, bluntly stated that this change reflects more of a withdrawal of arbitrage funds from hedge funds and large U.S. accounts rather than a shake in market confidence. In fact, the perpetual contract market represented by Binance, with its high-frequency settlement and flexible margin features, has long held the largest share of crypto derivatives trading volume. Even though CME has launched smaller denomination crypto futures contracts with a maximum duration of five years, it is difficult to reverse the trend of arbitrage fund outflow. This change in landscape is essentially a shift in the trading demand of the crypto derivatives market from singular arbitrage to a more diverse trading model that better fits market characteristics.

If the reversal of the exchange landscape is a superficial phenomenon, then the diversification of the asset structure in the crypto market is the deep core of this restructuring. The year 2025 will be a key turning point for the crypto market. As the global regulatory framework gradually clarifies, investor expectations in the crypto field continue to improve, and institutional funds have completely bid farewell to the era of 'only Bitcoin matters.' Data from CME Group shows that the average nominal open interest in its Ethereum futures has skyrocketed from $1 billion in 2024 to nearly $5 billion in 2025, with tokens like Ripple's XRP and Solana becoming new targets for institutional investment. This diversification of asset allocation has made the crypto derivatives market no longer reliant on the single volatility of Bitcoin, enhancing the market's risk resistance.

The maturity of the market has also given rise to a significant 'self-balancing effect.' The judgment of Le Shi, Managing Director of Auros in Hong Kong, is becoming a reality: as traditional participants have access to ETFs, direct access to exchanges, and other channels to express directional views, price differences between different trading venues continue to narrow, and the arbitrage space that boosts CME's open interest is naturally compressed. After the collective crash of crypto assets in October 2025, this effect was further amplified—despite the Federal Reserve's interest rate cuts reducing funding costs, the crypto market did not show a sustained rebound; borrowing demand weakened, DeFi yields remained low, and traders abandoned high-leverage one-way bets, opting for options and hedging tools as more stable trading methods. The market's leverage level has significantly declined, and speculative attributes have been notably reduced.

Currently, the crypto market is in a period of turbulence after this restructuring. On January 21, 2026, the price of CME Bitcoin futures fell by 2.8% to $87,488.8. The next day, it slightly rebounded to $90,376.75, but the short-term price fluctuations still reflect the market's adaptation process after bidding farewell to the arbitrage dividends. The views of Bohumil Vosalik, Chief Investment Officer of 319 Capital, are on point: the era of nearly risk-free high returns in the crypto market has ended, which will force high-frequency and arbitrage institutions to leave their comfort zones and turn to more complex trading strategies in decentralized markets.

Essentially, this major restructuring of the crypto derivatives market is not a market retreat, but an inevitable evolution from speculation-driven to value-driven, from singularity to diversification, and from wild growth to regulated maturity. The failure of cash and arbitrage strategies has washed away short-term arbitrage funds; changes in the exchange landscape adapt to the inherent trading demands of the crypto market; the diversification of asset structures solidifies the foundation for the long-term development of the market. When risk-free arbitrage dividends fade away, the crypto derivatives market truly enters a new era of competing professional capabilities, trading strategies, and risk control.

The restructuring of the crypto derivatives market continues. How will institutions layout complex strategies for decentralized markets in the future? What new trading opportunities will further clarity in regulation bring? We welcome everyone to leave their views in the comments section, and don’t forget to follow, like, and share this article to track the latest changes in the crypto market! #达沃斯世界经济论坛2026 #特朗普取消对欧关税威胁 #美国加密市场法案延迟 #下任美联储主席会是谁? #特朗普对欧洲加征关税 $BTC