Crypto Wash Sales Explained:

For most people who come into crypto from stocks, taxes are one of the first areas where things start to feel confusing. You hear that crypto is “property, not securities,” then you hear that you can sell at a loss and buy back immediately, and then someone warns you that this loophole could close any day. All of that is technically true, but the real picture is more nuanced than most short explanations make it sound.

Why the wash sale rule exists in the first place

The wash sale rule didn’t come from crypto. It came from traditional markets, long before digital assets existed.

In stocks, the rule exists to stop people from gaming the tax system. Without it, an investor could hold a stock that’s down, sell it on December 31 to lock in a tax loss, then buy the same stock back on January 2 and continue holding it as if nothing happened. On paper, they’d show a loss for tax purposes, but economically they never really exited the position.

To prevent this, U.S. tax law says that if you sell a stock or security at a loss and repurchase the same or a “substantially identical” security within 30 days before or after the sale, the loss is disallowed. You don’t lose it forever, but you can’t use it immediately. Instead, it gets added back into your cost basis.

That rule is very clear for stocks and securities. The confusion starts when people try to apply it to crypto.

Why crypto is different under current U.S. tax law

The key reason crypto wash sales are treated differently today is simple: the IRS classifies cryptocurrency as property, not as stock or securities.

The wash sale rule, written in Section 1091 of the tax code, applies specifically to “stock or securities.” Crypto does not fall under that definition as the law is written today. Because of that, the rule technically does not apply to Bitcoin, Ethereum, or other digital assets.

That’s why you’ll often hear the statement:

“Yes, you can sell crypto at a loss and buy it back immediately without losing the deduction.”

From a strictly legal standpoint, as of now, that statement is correct.

But “legal” and “wise” are not always the same thing.

What tax-loss harvesting looks like in the real world

Let’s step away from theory and look at how this actually plays out for normal investors.

Imagine a regular retail investor, not a hedge fund, who bought Ethereum at $3,800 during a bull run. Months later, ETH is trading at $2,200. The investor still believes in Ethereum long term, but they also had other trades this year that produced gains.

If this investor sells ETH at $2,200, they realize a capital loss. That loss can offset capital gains from other trades and, if losses exceed gains, up to $3,000 of ordinary income for the year. Any excess carries forward.

Under current rules, that investor could sell ETH, realize the loss, and buy ETH back the same day or the next day. The deduction still stands.

This is why crypto tax-loss harvesting became popular. It wasn’t invented to cheat the system; it simply followed the rules as they exist.

Why many investors still wait 30 days anyway

Even though immediate rebuying is allowed today, a large number of cautious investors choose not to do it. That might seem overly conservative at first, but there are good reasons behind it.

First, tax law changes often apply going forward, but audits look backward. If Congress extends wash sale rules to crypto in the future, the IRS may scrutinize past behavior more closely, especially if it looks aggressive.

Second, the IRS has not issued crystal-clear guidance saying “crypto wash sales are explicitly allowed.” The position is inferred from how the law is written, not from a direct blessing. That leaves room for interpretation, especially in edge cases.

Third, consistency matters. Investors who build habits that mirror traditional wash sale timing don’t have to suddenly change behavior if the rule expands. They’re already compliant by default.

This is why you’ll hear many tax professionals say something like:

“Yes, you can do it, but we don’t recommend making it a habit.”

The “substantially identical” problem in crypto

One of the trickiest parts of wash sale rules in traditional finance is the idea of “substantially identical” assets. With stocks, this is usually straightforward. Selling Apple stock and buying Apple stock again is clearly identical.

In crypto, it gets blurry.

Is selling Bitcoin and buying Wrapped Bitcoin substantially identical?

What about selling ETH and buying stETH?

What about rotating between two tokens that track the same index or ecosystem?

Right now, none of this is clearly defined in law for crypto. That uncertainty is another reason conservative investors prefer clean, defensible behavior rather than pushing boundaries.

If a wash sale rule is extended to digital assets, lawmakers will likely need to clarify these definitions. Until then, gray areas exist.

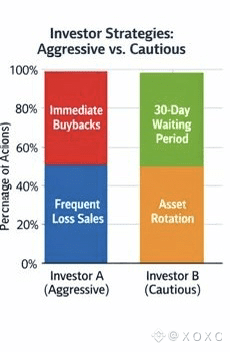

Realistic example: cautious vs aggressive behavior

Let’s compare two real-world styles of investors.

Investor A is aggressive. They sell a token at a loss on December 29, buy it back minutes later, and do this repeatedly across many assets. On paper, they generate large losses while barely changing their portfolio exposure.

Investor B is cautious. They sell a token at a loss, move into cash or a related but different asset, and wait at least 30 days before repurchasing the original token.

Both investors may be technically compliant today. But if rules change or audits happen, Investor B’s behavior is far easier to defend. It looks like genuine portfolio management, not tax engineering.

That distinction matters more than most people realize.

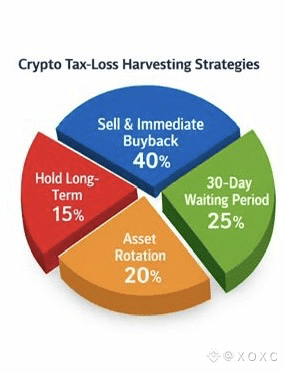

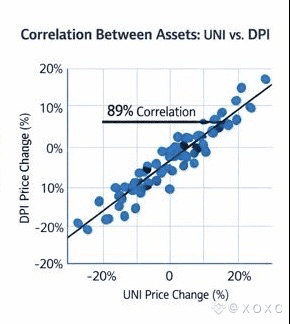

Correlated asset rotation: how it actually works

Correlated asset rotation: how it actually works

One practical strategy that many investors use is rotating into a closely correlated asset instead of rebuying the same one immediately.

For example, someone who sells UNI at a loss might rotate into a DeFi index token, or into ETH itself, if their thesis is broader than one protocol. The portfolio stays exposed to the sector, but the specific asset sold is not repurchased right away.

This mirrors what stock investors sometimes do when they sell one ETF and buy a similar but not identical one during the wash sale window.

Again, this is not about loopholes. It’s about risk management and defensibility.

Why lawmakers keep revisiting this issue

Since 2021, multiple U.S. tax proposals have included language that would extend wash sale rules to digital assets. None of them have passed into law yet, but the pattern matters.

The government is not ignoring this area. Each new proposal signals intent, even if political realities delay implementation.

From a policy perspective, the argument is simple: if crypto behaves like an investment asset and is used for tax-loss harvesting, lawmakers see little reason to treat it differently from stocks.

That doesn’t mean a rule change is guaranteed tomorrow. But it does mean assuming the loophole will last forever is risky.

How a rule change would impact everyday investors

If wash sale rules are extended to crypto, most casual investors won’t be dramatically affected. People who buy and hold for long periods, or who don’t aggressively harvest losses, will barely notice.

The biggest impact would be on frequent traders and those who systematically sell and rebuy the same tokens to generate paper losses.

For those investors, strategies would need to change. Waiting periods would matter. Asset rotation would become more important. Record-keeping would need to be tighter.

None of this would end tax-loss harvesting. It would simply make it more structured, similar to traditional markets.

Wash trading vs wash sales: an important distinction

Wash trading vs wash sales: an important distinction

A lot of people confuse wash sales with wash trading, but they are not the same thing.

Wash trading refers to artificially inflating trading volume by buying and selling the same asset to yourself or between controlled accounts. That’s a market manipulation issue, not a tax strategy. Regulators across the world generally frown on it, even in crypto.

Wash sales, on the other hand, are about taxes. They involve selling at a loss and rebuying, not to fake volume, but to manage taxable income.

Mixing these two concepts leads to unnecessary fear and misunderstanding.

What responsible behaviour looks like today

For most investors, responsible behavior doesn’t mean avoiding tax-loss harvesting entirely. It means using it thoughtfully.

That includes:

Understanding your cost basis clearly

Avoiding rapid, repetitive sell-and-rebuy cycles

Keeping detailed records

Being prepared to explain your strategy if asked

And most importantly, staying flexible. Crypto tax rules are still evolving, and rigidity is rarely rewarded in fast-changing regulatory environments.

The mindset that matters more than the rule itself

At the end of the day, the most important thing isn’t whether crypto has a wash sale rule today. It’s how you approach compliance and risk.

Investors who treat taxes as something to “outsmart” often end up stressed when rules change. Investors who treat taxes as part of long-term planning adapt more easily.

Waiting 30 days before rebuying isn’t about fear. It’s about building habits that remain valid even as the landscape shifts.

Final thoughts

So yes, it is true that crypto is not currently covered by the IRS wash sale rule. And yes, you can technically sell at a loss and buy back immediately without losing the deduction.

But reality is more layered than that headline suggests.

Cautious investors look beyond what’s allowed today and think about what will still make sense tomorrow. They focus on consistency, clarity, and defensibility rather than squeezing every last short-term advantage.

Crypto markets move fast, but tax authorities move slowly and deliberately. Bridging that gap with smart habits is usually the difference between confidence and constant anxiety.

If you approach crypto taxes with that mindset, rule changes become manageable, not scary.

#BTC #bnb #USIranStandoff #Binance #BinanceSquare $BTC @Daniel Zou (DZ) 🔶