1. The Illusion of Perpetual Growth: Contextualizing the Modern Market

In the current global financial landscape, the "buy and hold" mantra has ascended from a prudent investment heuristic to a near-religious dogma. However, this unwavering faith is currently navigating its most profound structural challenge since the Great Depression. For four decades, market participants have operated under the assumption of a permanent upward trajectory, largely disregarding the historical reality that long-term economic cycles eventually demand a fundamental reckoning. We are currently witnessing a period where the foundational mechanics of the market—and the psychological frameworks supporting them—are being strained by historic debt levels and an unprecedented lack of breadth.

To grasp the gravity of the current moment, one must analyze the market peak of 1929. Following that zenith, the equities market experienced a staggering 90% contraction over the subsequent three years. This was not merely a mechanical collapse of valuations; it was a psychological dissolution—a total "loss of belief" in the structural integrity of the markets. Today, this historical precedent has been largely erased from the collective memory, replaced by an over-reliance on the S&P 500 as an infallible vehicle for wealth generation.

Strategically, the S&P 500 should not be viewed as a mere diversified index, but rather as a "geopolitical bet" on U.S. hegemony and dollar-denominated supremacy. Investing in the index is an implicit wager on the continued expansion of the American economic model, the stability of cross-border capital flows, and the permanence of Western financial leadership. However, a granular analysis of the index’s current architecture reveals that this bet is no longer as diversified or as stable as retail sentiment suggests.

2. The Concentration Trap: Why "Diversification" is a Mathematical Myth

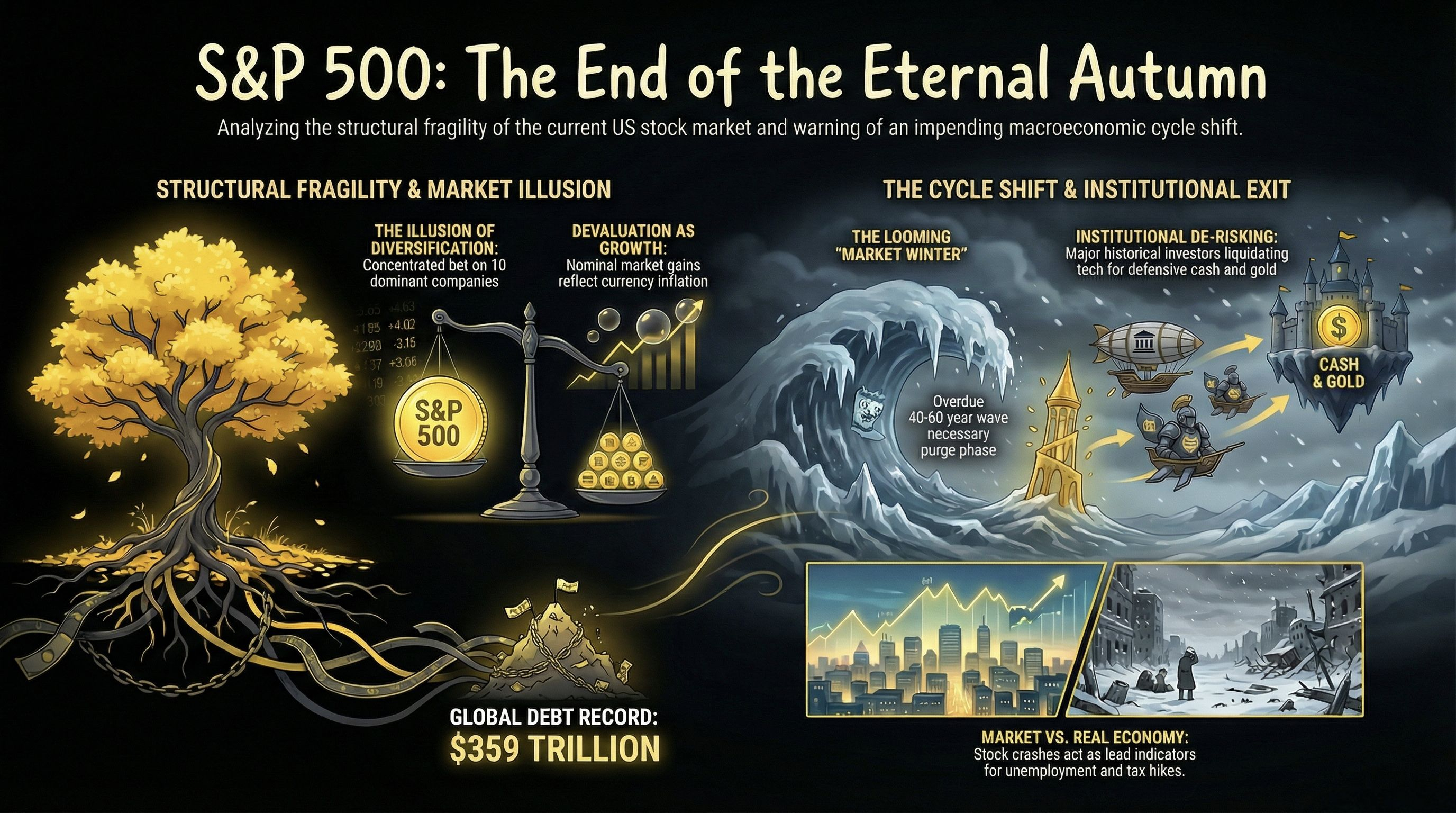

Strategic risk is frequently obscured by nominal success. Many modern investors operate under the illusion of diversification simply because they hold an index comprising 500 constituents. This is a mathematical fallacy in the current environment. The S&P 500 has transitioned from a broad representative cross-section of the industrial and service economy into an idiosyncratic concentration in mega-cap technology equities. When the performance of an entire national index is dictated by a decimal-point fraction of its members, the safety traditionally associated with indexing evaporates, leaving institutional and retail portfolios exposed to systemic failure should a handful of entities falter.

The "Magnificent" few—Apple, Microsoft, Nvidia, Google, Amazon, Meta, and Tesla—now exert a disproportionate influence on the index's direction. Rather than a broad-based economic wager, an S&P 500 position today is effectively a leveraged bet on ten companies. Since the 1980s, the ascent of this index has been sustained by several core pillars that are now exhibiting signs of terminal stress:

U.S. Global Hegemony: The central role of the United States in the global financial architecture is facing challenges from a transitioning multi-polar world.

The Dollar as Reserve Currency: The structural demand for the U.S. dollar is under pressure from "de-dollarization" trends and the increasing weaponization of the financial system.

Expansion through Debt: A growth model predicated on constant monetary expansion and the accumulation of $359 trillion in global debt, a level that strains the limits of fiscal sustainability.

The systemic implication for global portfolios is profound: if these ten pillar entities experience a valuation reset due to regulatory headwinds, technological disruption, or a contraction in earnings capacity, the primary vehicle for global retirement and institutional wealth risks a synchronized collapse. This concentration masks a more insidious reality: much of the apparent growth is not a reflection of fundamental productivity, but a byproduct of the persistent devaluation of the unit of account.

3. The Inflationary Veil: Growth vs. Monetary Devaluation

A cornerstone of sophisticated macro-economic analysis is the ability to distinguish between real intrinsic value and nominal price appreciation. Since the definitive abandonment of any serious monetary anchoring in the early 1980s, the U.S. dollar has undergone a structural loss of purchasing power. When the currency—the very yardstick of value—is devalued, the nominal prices of assets like equities appear to rise, creating an "inflation disguised as ROI" effect that lures the unwary into a false sense of prosperity.

The trajectory of the S&P 500 over the last forty years is, in significant measure, the result of this monetary debasement. While investors celebrate record nominal highs, they often ignore the volume of liquidity required to sustain those levels. This phenomenon has been meticulously managed by central bank interventions, creating what can be identified as an "Autumnal" market phase—a period of late-cycle euphoria where valuations have detached from fundamental earnings capacity due to artificial liquidity injections. Central bank manipulation can delay the arrival of the next phase, but historically, it has never been able to cancel the cycle itself.

4. The Four Seasons of Debt: Navigating the 40-60 Year Cycle

Long-term economic cycles, as analyzed by figures such as Milton Friedman and Ray Dalio, operate in waves of 40 to 60 years. Understanding the "seasonality" of debt and productivity is essential for capital preservation. Historically, these cycles progress through four distinct stages:

Spring (Productivity Growth): Real economic expansion driven by innovation and genuine productivity gains.

Summer (Inflationary Heat): Rising prices and the initial signs of systemic overheating.

Autumn (Financial Bubble): A period of extreme financial euphoria fueled by debt and speculative excess.

Winter (The Purge): A necessary phase of deleveraging and market correction that clears systemic inefficiencies and "zombie" entities.

Since the 1980s, global policy has been oriented toward the artificial extension of "Autumn." By utilizing extreme monetary policy and allowing global debt to balloon to a record $359 trillion, the financial authorities have blocked the arrival of "Winter." This debt now serves as a massive barrier to a healthy correction; the system has become so fragile that it cannot withstand the very purge it requires to reset.

We are currently observing the "Peter and the Wolf" phenomenon in market psychology. Because warnings of a correction have been issued for years without a terminal crash occurring, the investing public has become immunized to risk. This has led to a state of collective Complacency and Euphoria. Mapping the current market to the classic emotional cycle—which moves from Incredulity and Hope through to Optimism, Belief, Enthusiasm, and finally Euphoria—it is clear we are in the terminal stages of the latter. In this phase, the perceived risk is at an all-time low precisely when the systemic risk is at an all-time high.

5. Following the Smart Money: Signal vs. Noise

Strategic educators prioritize institutional "insider" sentiment over retail euphoria. While the general public is encouraged to maintain aggressive exposure, the architects of the last forty years of growth are conspicuously repositioning. Warren Buffett, perhaps the most consistent value investor in history, has been aggressively accumulating cash, signaling a lack of long-term value in current equity valuations. His current cash position is a direct reflection of the "Buffett Indicator" (Market Cap to GDP) signaling extreme overvaluation and a high opportunity cost for capital.

Furthermore, investment luminary Stanley Druckenmiller has executed a significant forward-looking positioning move, divesting roughly 70% of his technology and S&P positions as of early 2025. His firm has simultaneously pivoted toward defensive "refuge" assets, specifically gold-mining equities such as Barrick Gold and Newmont. The critical question for the sophisticated investor is: why are the individuals who generated billions from the S&P 500’s ascent choosing this specific juncture to exit? Their migration to gold and cash suggests the risk-to-reward ratio for broad indices has turned decisively negative.

6. The Ripple Effect: Why the "Non-Investor" is Still at Risk

It is a dangerous misconception to believe that one is insulated from equity market volatility by non-participation. The health of the S&P 500 is inextricably linked to the "Economy of the Street." The index functions as a global commander; its movements dictate international fiscal policy and national tax regimes with far more authority than any local politician. In practical terms, the U.S. stock market mandates the direction of European policy 100 times more effectively than a leader like Pedro Sánchez.

When the S&P 500 undergoes a significant correction, the consequences are felt in the real economy:

The 2008 Crisis: A 60% decline in the S&P 500 translated into a global collapse in employment, business insolvency, and a decade of fiscal austerity and tax hikes.

The 2020 Shock: A 34% contraction in a single month served as the precursor to massive state intervention, business closures, and the subsequent rampant inflation that currently erodes the purchasing power of every household.

Job security, pension solvency, and the price of basic goods are all derivatives of this system. A crash in the S&P 500 is not merely abstracted digital volatility on a screen; it is a catalyst for economic hardship, manifested in reduced opportunity and increased state-driven wealth extraction through taxation.

7. Strategic Reflection: Wealth Preservation in a Changing Paradigm

The current market euphoria is a classic symptom of a late-stage "stretched Autumn." The signals of an impending "Winter" purge—from record debt to insider selling—are being ignored in favor of the comfort of the status quo. However, the laws of economic seasonality are indifferent to optimism. The transition from a period of artificial expansion to one of systemic deleveraging is not a matter of "if," but "when."

This is not a call for panic, but a requirement for rigorous strategic reflection. The objective of the coming decade is not the pursuit of speculative returns, but the protection of the fruit of one’s lifetime of effort against the triple threats of inflation, taxation, and financial manipulation. The global economic landscape is shifting rapidly, and those who rely on the dogmas of the last forty years—the era of the easy dollar—will find themselves ill-equipped for the next ten.

In an era of institutionalized manipulation, intellectual autonomy is the only hedge against systemic insolvency. Recognizing that the S&P 500 is no longer a diversified safety net, but a concentrated geopolitical bet, is the first step toward genuine capital preservation. As the cycle inevitably turns toward its winter phase, the priority must shift from following the herd to securing one's financial future against a paradigm that is already beginning to fracture.