Bitcoin’s on-chain P&L structure has shifted, but it has not broken. Spot trades near $88k, while the realised price sits around $56k, so the representative holder remains comfortably in profit. Price is no longer parabolic, yet it still sits almost 60% above the aggregate on-chain cost basis, a compression of profitability, not its destruction.

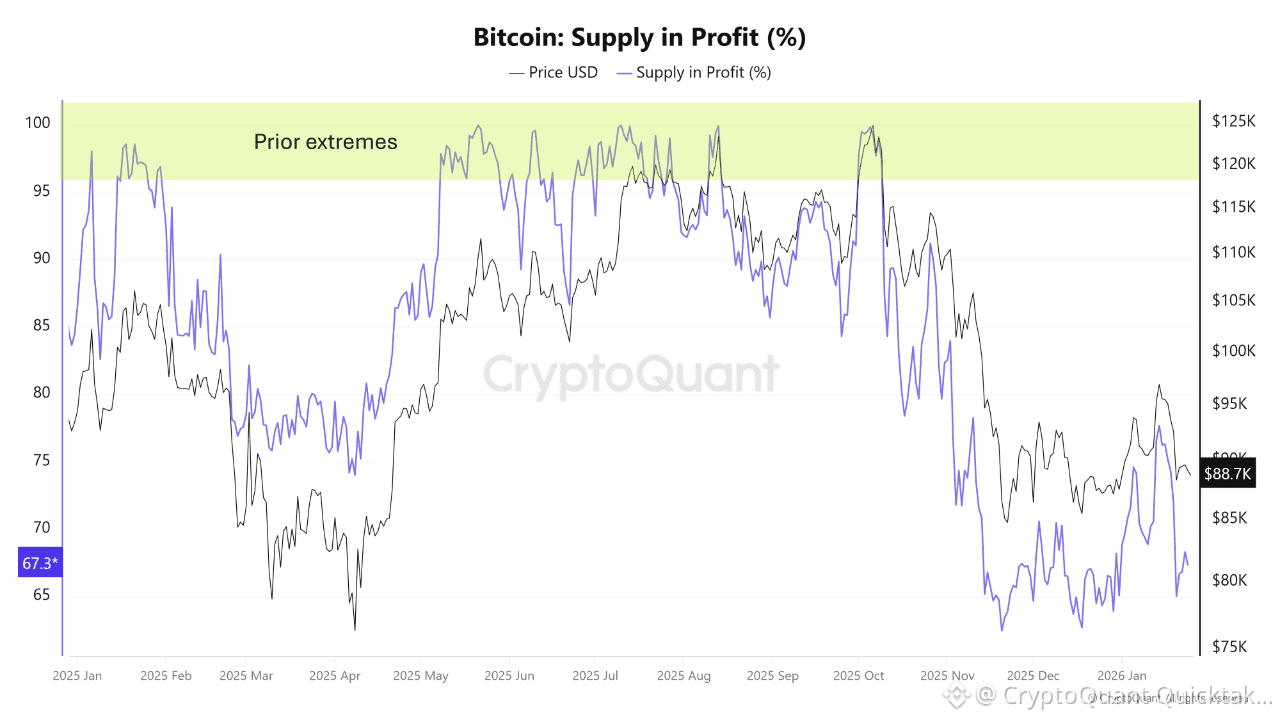

That compression is most visible in breadth. Roughly two-thirds of the supply remains in profit, and one-third now sits in loss. Earlier in the year, almost every coin was in the green; now, a meaningful minority is underwater and therefore more price-sensitive. However, these loss levels are still far from the 80–90% extremes that have historically marked cycle lows.

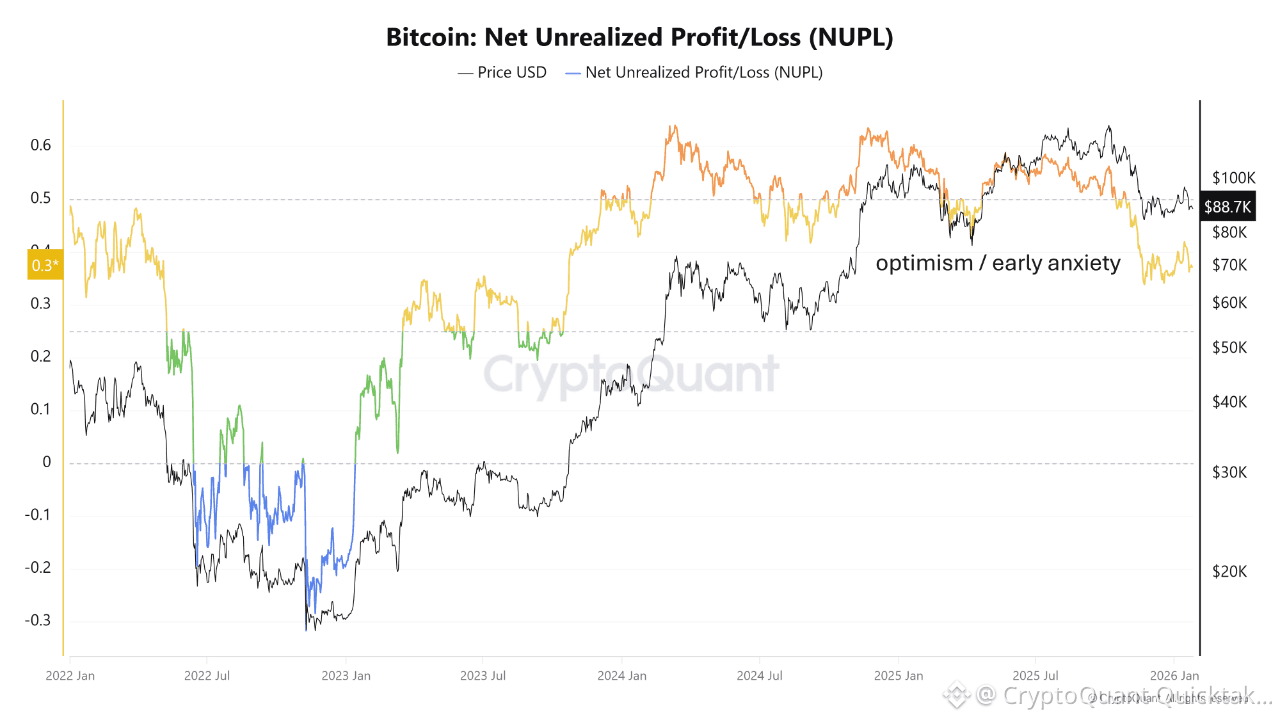

Valuation has also normalised. The MVRV ratio has cooled to about 1.5x, well below the 3–4x “blow-off” band but above the sub-1x levels that have historically signalled deep value in prior bears. NUPL tells a similar story: the market has migrated from euphoria into an “optimism/anxiety” zone where gains exist, but conviction is weaker.

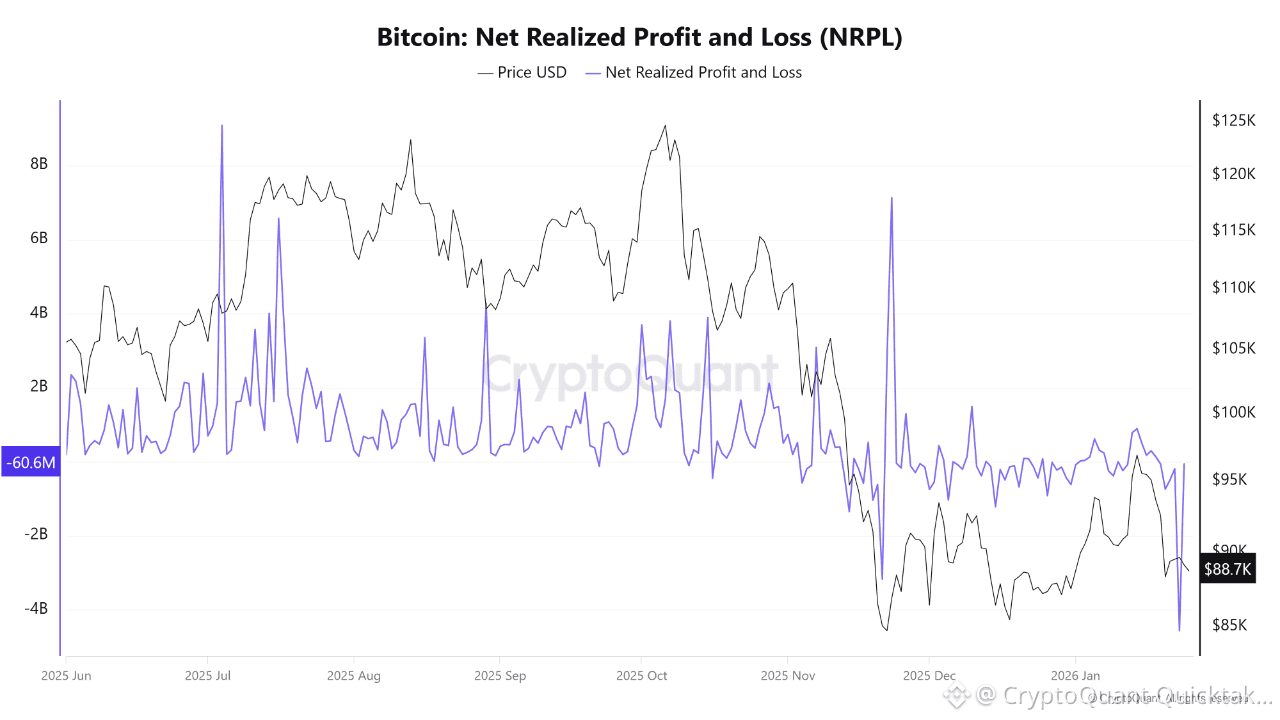

Finally, Net Realised Profit/Loss has flipped from persistent profits to choppy, modest losses. Realised P&L now prints negative often enough to matter, but we have yet to see the sustained, outsized loss spikes that typically signal broad capitulation.

Taken together, these signals describe an early-bear or digestion regime: profit cushions are thinner, stress is building at the margin, but the cycle has not fully reset. For professional allocators, this backdrop argues for smaller net-long exposure, greater use of relative-value and volatility strategies, and patience in waiting either for renewed momentum or for a clearer capitulation opportunity.

Written by Novaque Research