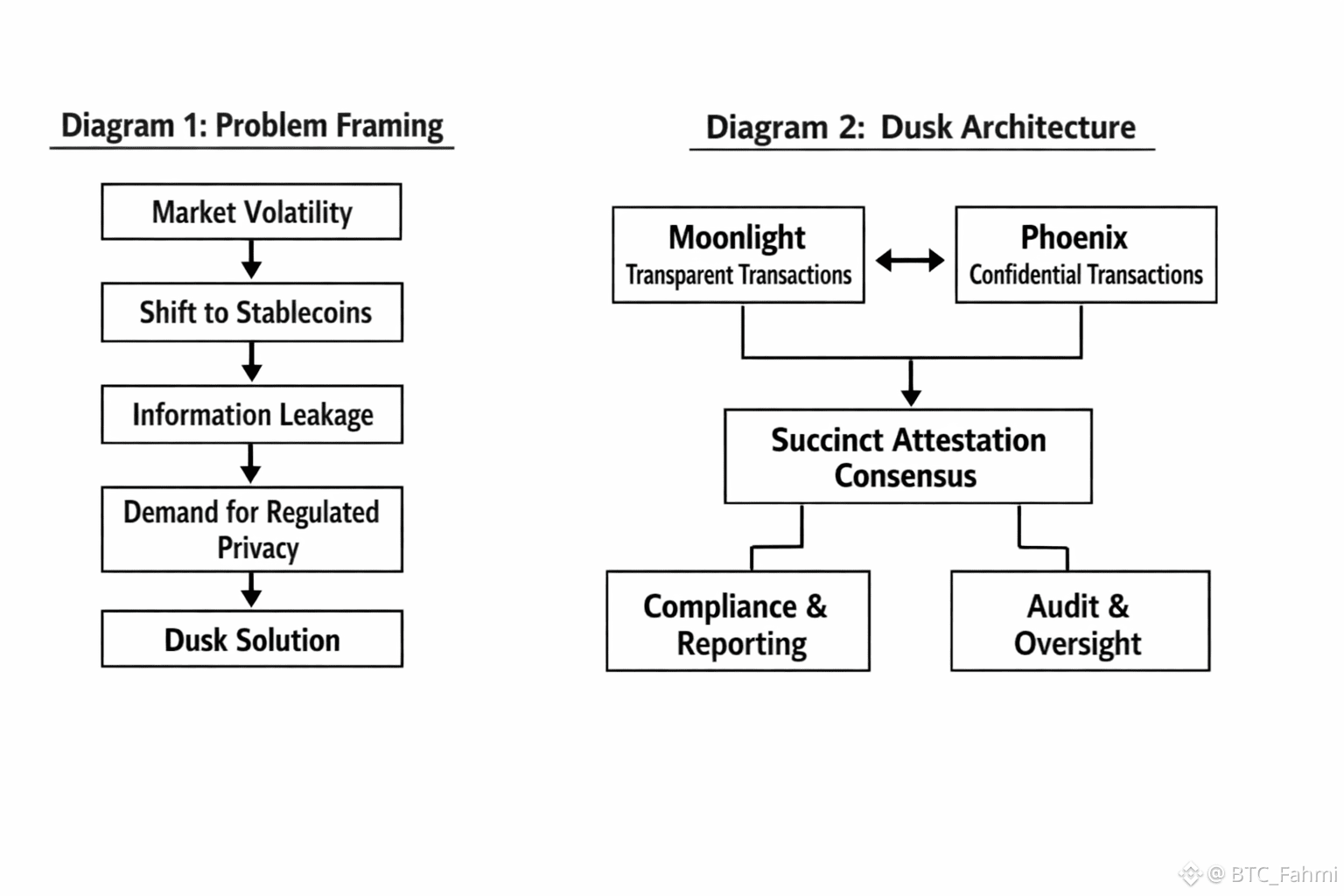

When I first looked at Dusk, it was because a familiar argument about privacy started sounding wrong. In crypto circles, privacy is often treated like a moral stance, either you want radical transparency or you want to disappear. But in actual finance, privacy is mostly operational. If you remove it, you do not get “more honesty,” you get broken market structure.

That gap is easier to see in the current tape. Bitcoin is trading around $89,487 today, with an intraday range of roughly $87,271 to $90,276 and ETH is around $3,012 with its own sharp daily swings. In a market that jumpy, more flows move into stablecoins, and the stablecoin layer keeps getting heavier. Data cited off DeFiLlama has stablecoin market cap peaking around $311.3 billion in mid January and sitting near $309.1 billion recently, which is not a vanity metric, it is liquidity choosing a resting place.

That weight creates a second-order problem that most people still underprice. Payments and settlement are becoming onchain behaviors, but regulated institutions cannot operate on rails where every counterparty relationship, balance movement, and position change becomes public telemetry. Banks are already treating stablecoins like a deposit competitor, with Standard Chartered warning U.S. banks could lose as much as $500 billion in deposits to stablecoins by 2028. If that shift holds, more regulated money will touch blockchains, and the demand will not be “privacy or compliance.” It will be both, at the same time, in the same workflow.

This is the part Dusk seems built around: regulated privacy as a default stance, not a bolt-on feature. The simplest way to say it is that Dusk tries to copy the real rule of finance. Transactions are private to the public, but auditable to the right parties under the right process. Dusk’s design does not pretend that regulators will go away, it assumes they will arrive earlier than expected.

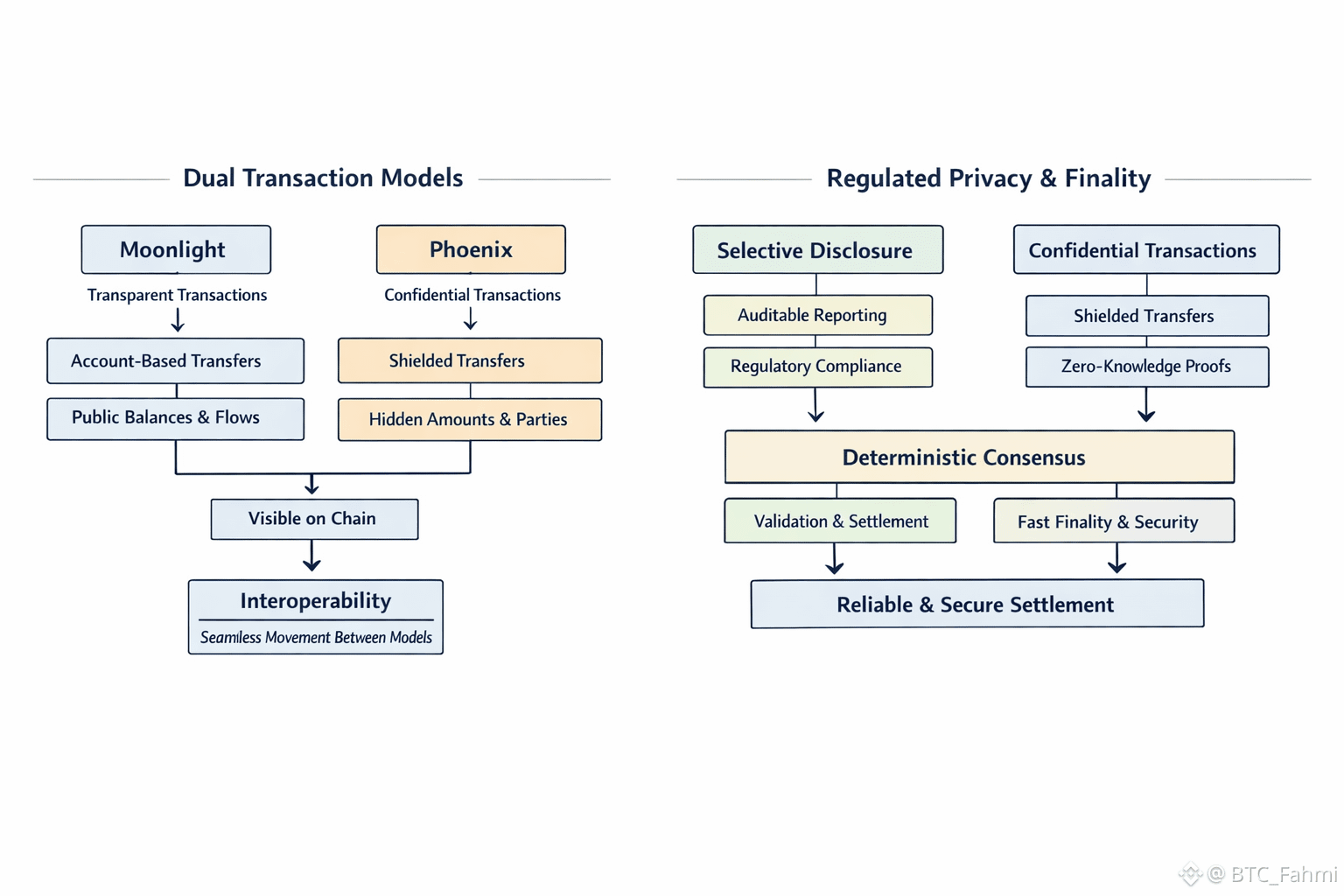

Underneath that framing is a practical architecture choice that matters more than the slogans. Dusk uses two transaction models: Moonlight for transparent, account-based flows, and Phoenix for confidential flows that behave more like shielded notes than public balances. Dusk’s own engineering materials describe Moonlight as fully transparent and account-based, and explicitly compatible with Phoenix so users can move between the two models. That is a quiet but important distinction, because most privacy systems force you into a separate universe where liquidity and compliance tooling do not follow.

On the surface, Phoenix looks like what people expect from privacy tech: hide amounts and relationships, keep the public chain from turning into a surveillance feed. Underneath, it is more rigid than people think, because “private” still has to be correct. Dusk’s own Phoenix materials describe confidential outputs living in a Merkle tree where spending requires proofs of inclusion and knowledge, so validity can be shown without exposing the sensitive parts. In plain language, the chain can verify that money is not being created or double spent, even if the chain cannot see who paid whom and how much.

The reason Dusk pairs that with Moonlight is not philosophical, it is about selective visibility. There are legitimate financial actions where transparency is required: issuance disclosures, reporting flows, regulated asset settlement that needs observable state, integrations with compliance systems that assume account models. Dusk’s documentation even frames wallet profiles as a pair of accounts, one “shielded” for Phoenix and one “public” for Moonlight, which is a direct admission that regulated finance is mixed by nature. If this works in practice, it lets the same chain host both confidentiality and the kinds of disclosures institutions cannot avoid.

Privacy is only half the story though. The other half is settlement certainty, because regulated finance does not like probabilities. Dusk anchors on deterministic finality through its Succinct Attestation consensus, described in Dusk’s docs as a permissionless, committee-based proof-of-stake protocol where randomly selected provisioners propose, validate, and ratify blocks to get fast deterministic finality. That sounds like consensus jargon until you connect it to an operational reality: clearing and settlement systems are built around “final” as a hard boundary, not a moving target.

This is where the “regulated privacy” idea becomes more than a privacy pitch. Confidentiality without reliable finality still leaves institutions with reconciliation risk. Reliable finality without confidentiality still leaves them with information leakage risk. Dusk is trying to close both gaps at once, which is rare, and also why the risk surface is wider than people admit.

You can see the ambition in the numbers the project is willing to put next to its roadmap. Dusk’s tokenomics documentation lists an initial supply of 500,000,000 DUSK, with another 500,000,000 emitted over 36 years, for a maximum supply of 1,000,000,000, and it notes the ICO raised $8 million in November 2018 at $0.0404 per token. Those figures matter because long emission schedules and staking incentives can keep validators aligned, but they also create an inflation overhang that the market has to absorb with real usage.

And real usage here is not just DeFi TVL chasing yields. Dusk has been tying itself to regulated asset narratives, including work with NPEX and references to bringing €300M AUM on-chain. If that pipeline produces actual settlement flows, the chain’s privacy and finality properties are no longer abstract. They become part of a business process that has auditors, reporting cycles, and liability.

Still, there are obvious counterarguments, and they are not weak. Privacy tech attracts regulatory suspicion even when it is designed for selective disclosure, because outsiders cannot easily tell the difference between “confidential” and “untraceable.” There is also a product risk: dual transaction models can confuse users and developers, and anything involving zero-knowledge proofs tends to increase complexity in tooling, debugging, and performance tuning. Even if the cryptography holds, the ergonomics might not, and finance is allergic to workflows that feel fragile.

There is also a market structure risk that shows up quietly. If too much activity stays in a shielded lane, you can starve public liquidity and price discovery. If too much activity stays public, you lose the very confidentiality institutions came for. The equilibrium is not automatic, it has to be designed, and it remains to be seen whether users will choose the “right” lane without making mistakes that create compliance problems.

The timing is what makes Dusk interesting right now. Stablecoins are growing into the plumbing layer, and the largest issuers are acting more like financial institutions themselves. Reuters reported USDT circulation around $186 billion, alongside Tether’s moves to allocate more into gold and hold large physical reserves, which is a reminder that the center of gravity is shifting toward regulated questions and balance sheet credibility. If onchain finance is becoming more bank-like, then the infrastructure it uses will be judged by bank-like standards: confidentiality, auditability, and settlement certainty.

So the bigger pattern here is not “privacy coins are back.” It is that the market is slowly relearning why finance was private in the first place. Public ledgers are a useful foundation, but they are not a full financial system on their own. If Dusk’s approach holds, it suggests the next wave of Layer 1 differentiation is not just speed or fees, it is how well a chain can express real-world constraints without leaking real-world information.

The observation that sticks for me is simple: transparency is a feature, but confidentiality is the default setting of serious money, and any chain that wants regulated finance has to build around that truth instead of arguing with it.