In this analysis, I will deconstruct the current wall of fear by examining the core indicators that form the true bedrock of the market. I will cut through the noise to argue that despite the palpable anxiety, the underlying fundamentals are robust. This panic, I believe, is an opportunity, not an omen.

Deconstructing the Wall of Fear: Anatomy of a Market Panic

The first step in any contrarian analysis is to quantify the prevailing sentiment. While fear is an emotion, its expression in the market has measurable characteristics. A look at the headlines, the media, and social media chatter reveals one thing: intense, pervasive fear.

A close examination reveals a panic engineered for maximum psychological impact:

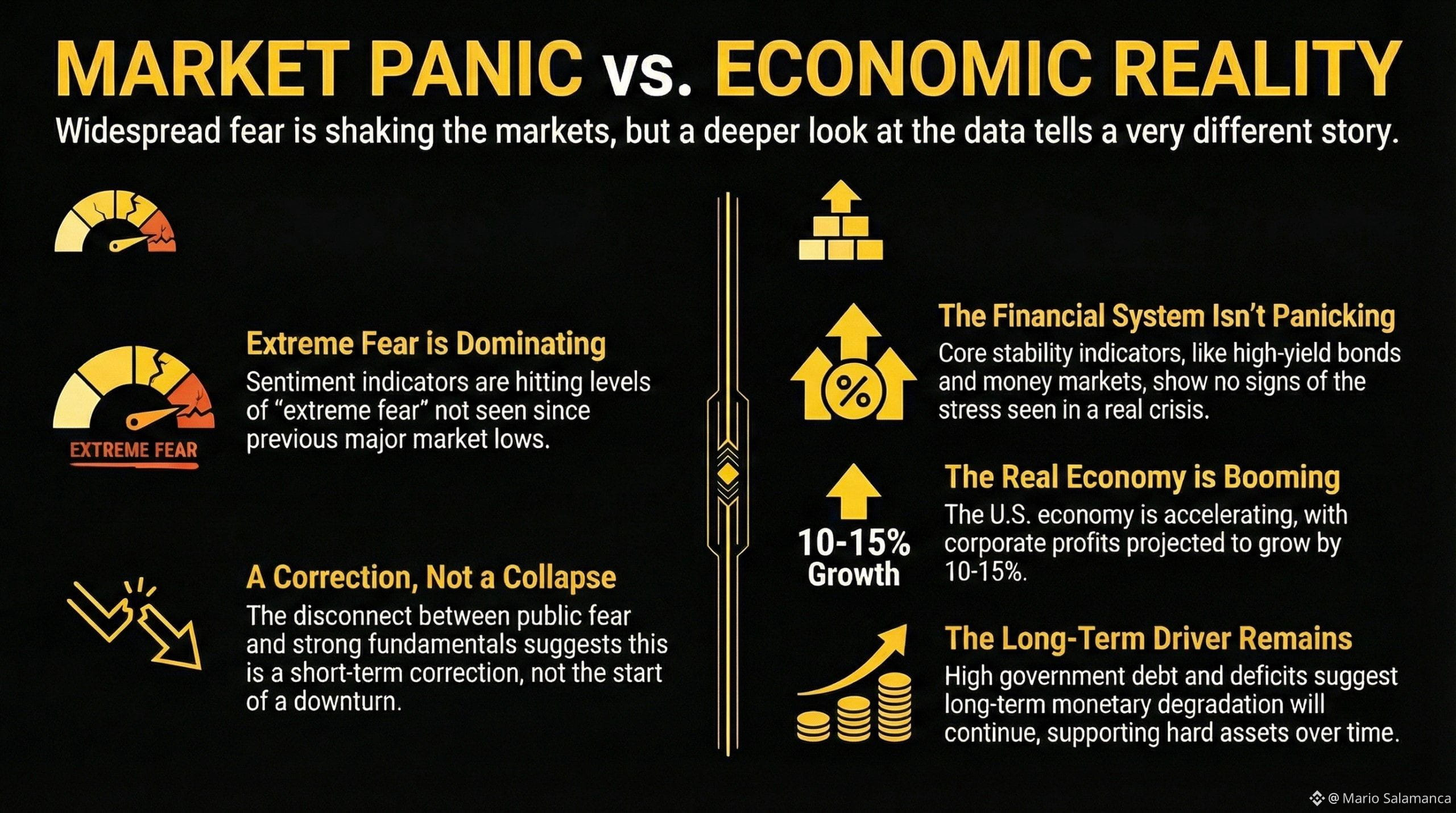

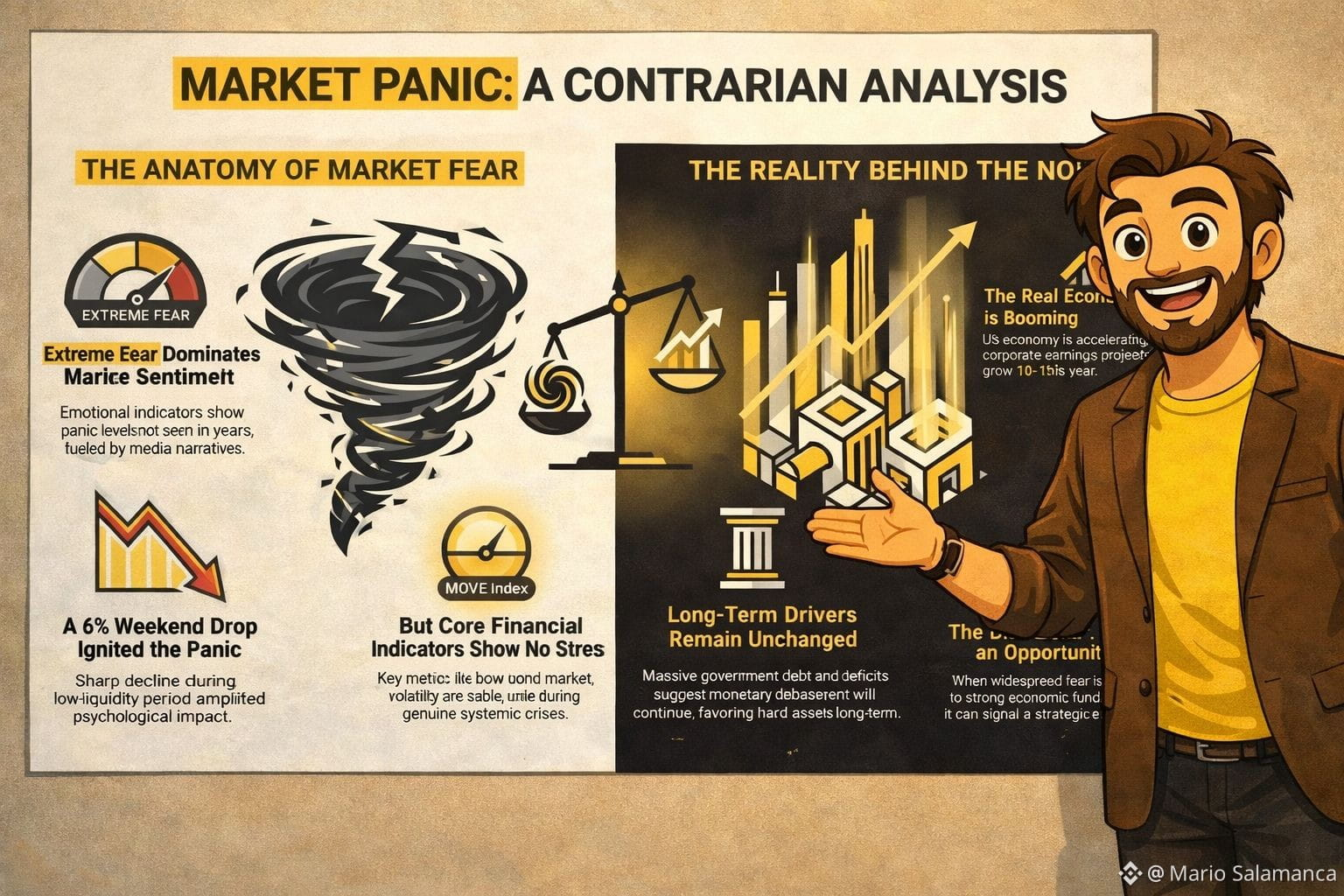

Extreme Fear Readings: Sentiment indicators, particularly for assets like Bitcoin, are flashing "extreme fear." These are readings comparable to those seen during significant market lows in previous years, signaling a level of pessimism that often precedes a reversal.

Technical Overselling: Key technical indicators confirm this emotional exhaustion. The 14-day Relative Strength Index (RSI) for Bitcoin, for instance, has plunged below 24, a deeply oversold condition not seen since 2022. This suggests the selling pressure has reached an unsustainable extreme.

Low-Liquidity Amplification: The timing of a recent, sharp 6% price drop in Bitcoin was no accident. It was executed over a weekend, a period of minimal market liquidity. This maneuver was designed to trigger a cascade of stop-loss orders and force liquidations, manufacturing a sense of crisis far greater than the event's fundamental importance.

This anatomy of fear reveals a narrative driven more by technical manipulation than by substantive decay. I’ll tell you the truth: before writing this, I bought Bitcoin. This fear is manufactured. To see the reality, we must ignore the noise and inspect the engine room of the financial system.

The Fundamental Reality Check: Why the Financial Bedrock Is Not Cracking

In moments of acute panic, a strategist's first move is to ignore the headlines and analyze the financial system’s core plumbing. The monetary and fixed-income markets are the ultimate arbiters of systemic stress; if a true crisis were unfolding, the strain would appear here first. A dispassionate review reveals not stress, but stability.

Calm in the Monetary Markets There are zero signs of liquidity stress in the short-term funding markets—the lifeblood of the banking system. The spread between the one-day repo rate and the effective federal funds rate is near zero, indicating banks are lending freely. This calm persists despite a bank having just been taken over by U.S. financial authorities. If there were real fear, this is where it would show up. It hasn’t.

Stability in the Bond Market The bond market tells an even more powerful story. Gold is falling. Silver is falling. The S&P 500 has fallen. And what are high-yield corporate bonds—the so-called "junk bonds"—doing? They are holding steady in a lateral range within a broader uptrend. If the market truly anticipated a severe economic downturn, these bonds would be plummeting. And they want to scare me with this? Come on. Furthermore, while headlines shout about stock volatility, the MOVE index—which measures volatility in the multi-trillion dollar U.S. Treasury market where the "smart money" lives—is in a clear downtrend. The professionals are not panicking.

Supportive Financial Conditions Broader measures confirm this lack of stress. The Chicago Fed's National Financial Conditions Index is below zero and trending lower. A reading below zero signifies "loose" financial conditions—the opposite of the tight, restrictive environment that precedes recessions.

The Key Signal from 2-Year Notes Perhaps the most telling signal comes from the 2-year U.S. Treasury note, which is highly sensitive to imminent economic trouble. Its yield remains contained at a key support level and has not broken its overarching bearish trendline. This demonstrates that the most informed participants in the world do not foresee a crisis that would force the Fed into an emergency response.

This is pure noise. With the financial system showing no signs of cracking, we can confidently turn to the positive momentum building in the real economy.

Beyond Finance: The Strength of the Real Economy

While financial markets are driven by short-term sentiment, the long-term driver of asset values is the health of the real economy and corporate profitability. The current bearish narrative directly contradicts the compelling evidence of economic acceleration.

A Booming U.S. Economy: The U.S. economy is not just growing; its rate of growth is accelerating. The data points to an economic boom, providing a powerful tailwind for corporate America.

Positive Growth Signals: This strength is corroborated by the U.S. Treasury yield curve. The spread between 10-year and 2-year yields is positive, a historically reliable forecast of economic expansion in the months ahead.

Robust Corporate Earnings: This economic vitality is expected to translate directly into strong corporate profit growth. Projections are for earnings to increase at a healthy rhythm of 10% to 15%.

And they’re telling me I should be bearish? What are you telling me? Don't mess with me. The narrative of an imminent crash clashes with the reality of an accelerating economy and surging corporate profits. The only identifiable headwind is a temporary drain on liquidity from an increase in the U.S. Treasury's account at the Fed. This positions the current weakness not as a new bear market, but as a transient "corrective phase."

The Long-Term Imperative: Why Monetary Debasement is the Endgame

A complete strategic assessment requires looking beyond immediate market moves to the structural realities of government finance. Here, the long-term trend is undeniable: the perpetual debasement of currency. Regardless of who leads the Federal Reserve, the fiscal mathematics of the U.S. government makes continued liquidity injection an inevitability.

The Political Agenda: The market expects any new Fed leadership will be pressured to foster aggressive economic growth, with targets as high as 6-7%. Such an agenda demands low interest rates.

The Fiscal Reality: These are the non-negotiable facts: a U.S. public deficit running at 6-7% of GDP and a national debt exceeding $40 trillion and growing.

The Inevitable Conclusion: I don't care about your theories or your models. Faced with this fiscal backdrop, any Fed chairman, whoever he may be, will be forced to monetize the debt. He will have to inject liquidity into the system and suppress interest rates to keep the government solvent. This is not a policy choice; it is a mathematical certainty. Monetary debasement will continue.

This powerful, long-term reality provides the ultimate context for interpreting short-term market volatility.

Conclusion: The Contrarian's Mandate

The evidence is clear. Today's market fear is a temporary phenomenon, a product of manufactured sentiment and short-term liquidity factors. It stands in stark contrast to the reality of a stable financial system, an accelerating economy, and the unavoidable long-term tailwind of monetary debasement.

They try to scare me? I've gotten older and I've seen this before. In an era defined by structural debt, I see these periods of intense, manufactured fear not as threats, but as gifts. They are valuable opportunities for the rational investor to separate the signal of long-term value from the noise of short-term panic. The mandate is to use these moments of collective anxiety to accumulate hard assets at a discount from panicked sellers. It's as clear as day.