Dusk is easiest to understand if you ignore the “blockchain” framing and look at the operational problem it’s trying to solve.

In real financial markets, transparency is not an abstract virtue. If every balance, trade, and counterparty relationship is public, you leak strategy, solvency signals, and pricing power. At the same time, regulators require systems to be provably correct, auditable, and capable of producing disclosures on demand. Most public chains fail immediately on the first requirement; most private systems fail on the second. Dusk exists in that gap. What it is really trying to offer is not privacy as a value statement, but confidentiality as infrastructure, combined with verifiability as a control mechanism.

This distinction matters because it narrows the scope of what Dusk can realistically be good at. It is not optimized to be a general playground for every kind of application. It is trying to be credible settlement infrastructure for workflows where information leakage is expensive and compliance is non-negotiable. If that market does not materialize, the design loses its reason for being.

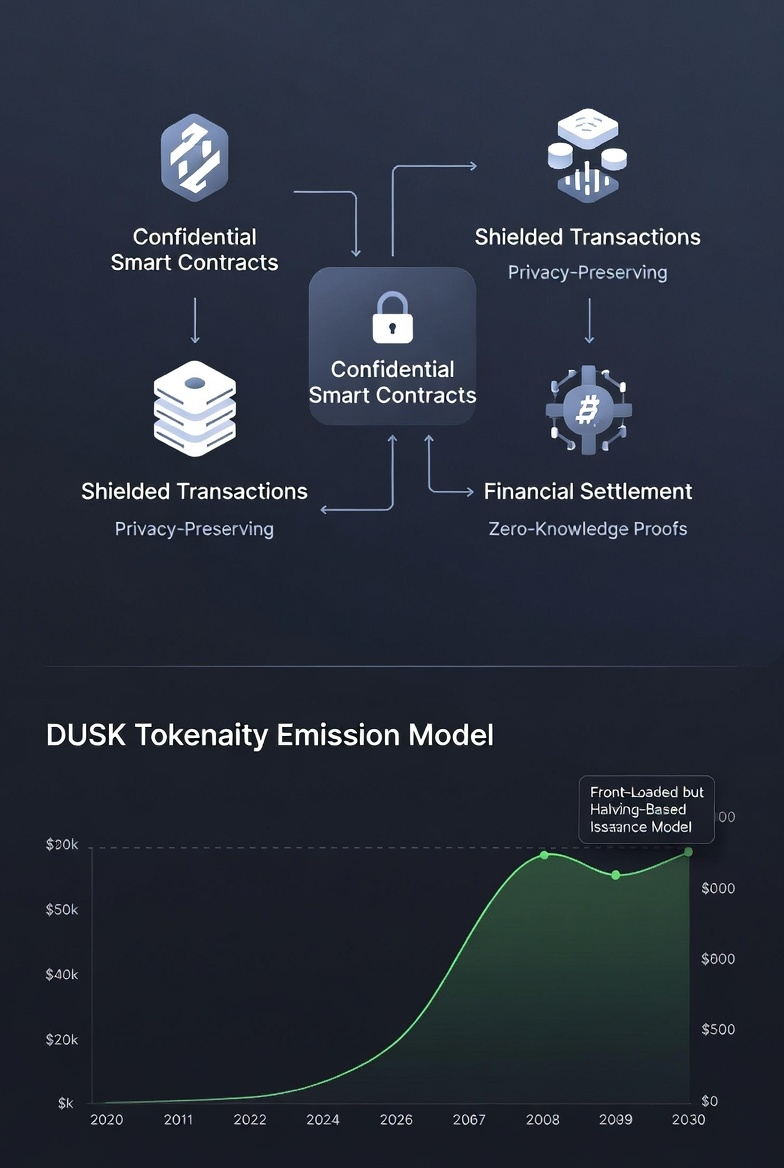

The technical design reflects that choice. Dusk’s base layer is built around deterministic finality and a transaction model that allows both public and shielded transfers. The shielded model is the core of the system: it allows value to move without exposing balances or flows, while still enforcing correctness through zero-knowledge proofs. This is the hard part of the design, and it carries real costs. Tooling becomes more complex, composability becomes less trivial, and the surface area for bugs and user error increases. Dusk is deliberately accepting that complexity because the alternative—full transparency—is structurally incompatible with many financial use cases.

Finality is treated as a first-order concern. From a finance perspective, probabilistic settlement is operational risk, not a philosophical feature. Deterministic finality makes sense if you want a chain to be used for issuance and settlement rather than speculation. The trade-off is that committee-based proof-of-stake systems depend heavily on stake distribution and coordination assumptions. Early on, these systems can be technically permissionless while still being economically concentrated, which weakens the “neutral infrastructure” claim until usage and stake distribution broaden.

There is also a tension in how Dusk approaches adoption. The project wants access to the existing developer ecosystem, which is why it supports an EVM environment. That environment, however, currently inherits delayed finalization semantics from its rollup architecture. This creates a mismatch: the base layer is designed around fast, deterministic settlement, while the environment where most applications would live does not yet fully reflect that property. This is not a fatal flaw, but it is a real gap between the core thesis and the user-facing execution layer. Whether that gap is temporary or structural will matter a lot.

The DUSK token is not ornamental. It is used for staking, it underpins the consensus mechanism, and it is the unit in which fees are ultimately paid. Removing the token would require redesigning the system’s security and incentive model. In that narrow sense, the token is necessary. But necessity alone does not create durable value. A token can be essential to protocol mechanics and still fail to capture value if demand is driven primarily by emissions rather than usage.

This is where the economics become uncomfortable. Dusk’s issuance schedule is front-loaded, with significant emissions in the early years to bootstrap security and participation. That is a rational design choice, but it creates sustained sell pressure unless it is offset by real fee demand. If most rewards are earned through inflation and sold to cover operating costs, staking becomes an inflation recycling mechanism rather than a reflection of underlying economic activity.

The long-term health of the token therefore depends almost entirely on whether the network begins to generate meaningful, recurring usage. Fee revenue, transaction volume tied to real assets, and sustained on-chain activity matter far more than total supply numbers or vesting schedules at this stage. Engineering progress is necessary, but it is not sufficient. Many projects ship code; very few create economic gravity.

Dusk’s defensible position, if it succeeds, is narrow but real. It is trying to be the place where private but auditable financial activity actually makes sense on a public network. Most chains either expose too much information or rely on off-chain confidentiality assumptions. If Dusk can make confidential settlement with selective disclosure cheaper and cleaner than building custom solutions elsewhere, it earns a reason to exist that is hard to replicate.

The unresolved question is whether that technical capability turns into adoption. The token does not become valuable because it is required by the protocol; it becomes valuable only if external actors need to acquire and stake it to access settlement capacity they cannot easily replace. If Dusk reaches that point, DUSK stops being an inflation-backed security token and becomes collateral for a network that people depend on. If it does not, the system can remain technically sound while the token’s value capture remains structurally weak.

In the end, Dusk’s viability is not about narratives or market cycles. It comes down to a single transformation: moving from a network that pays for its security by issuing tokens to one that is paid for by users who actually need what the network provides. That shift, if it happens, will not be subtle. It will show up in fees, activity, and sustained demand for stake. If it does not, no amount of design elegance will compensate.