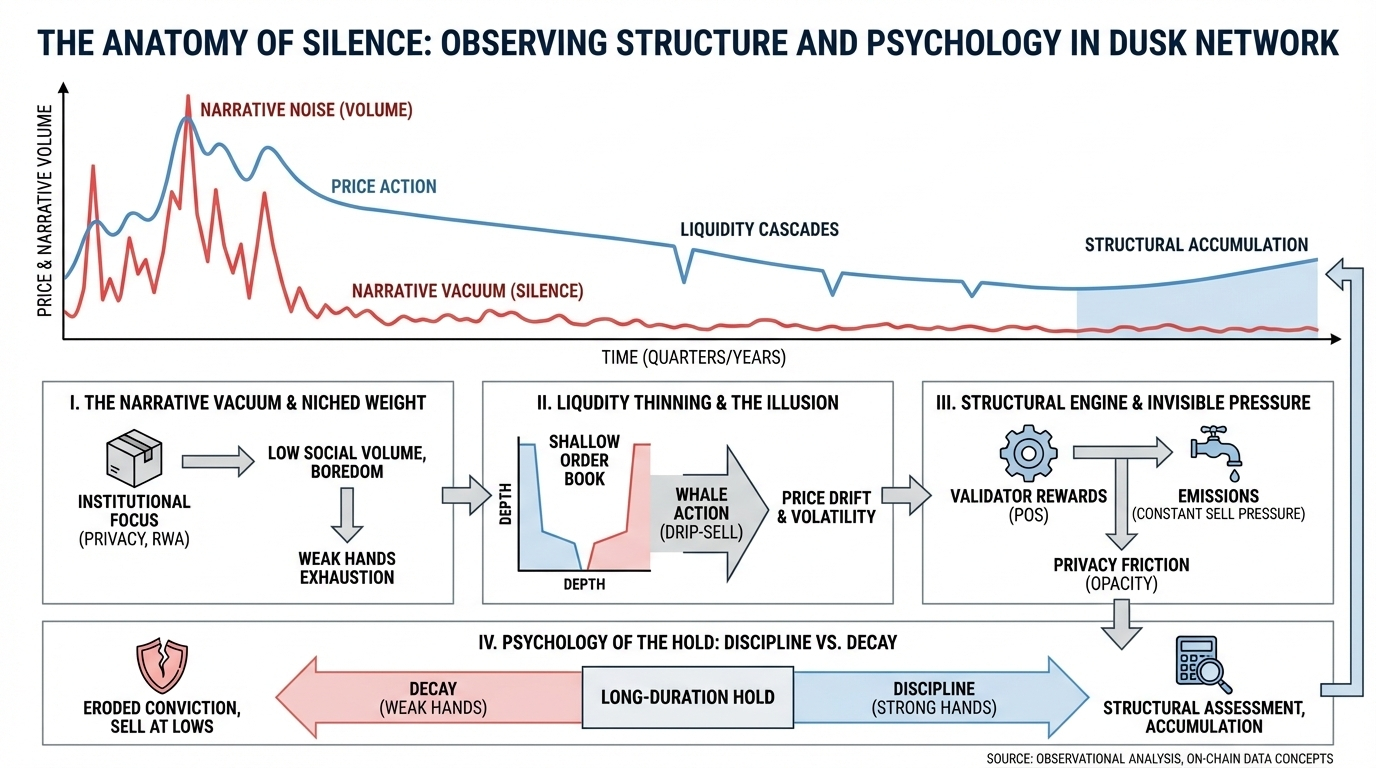

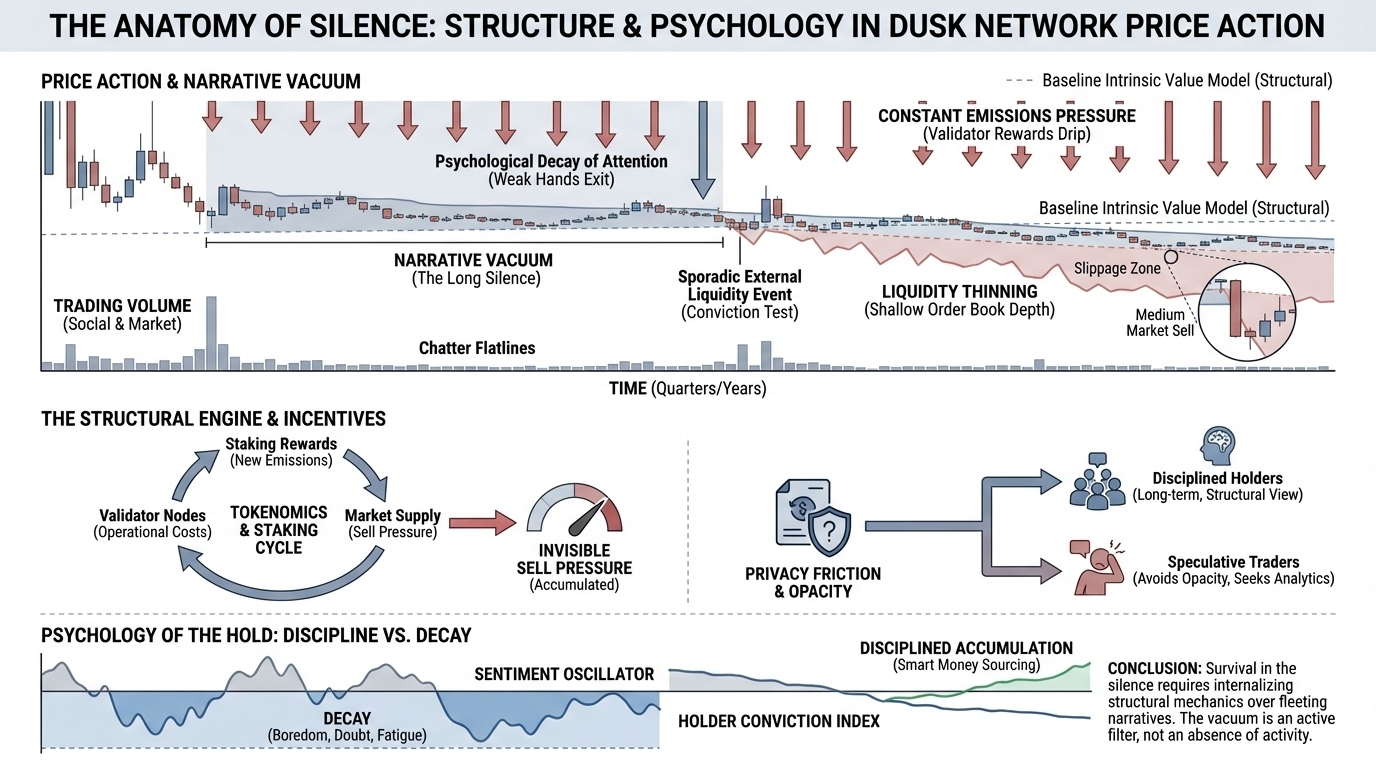

In crypto, noise is a commodity. Narratives are manufactured, amplified, and traded with a velocity that often outstrips the underlying technology. To observe a project like Dusk Network is, therefore, to engage in a study of contrasts. It presents a profound technological thesis privacy-enabled, regulated financial infrastructure wrapped in the brutal, often indifferent mechanics of crypto market structure. My interest lies not in the promise, but in the price action. Specifically, how it behaves during the long, unremarked periods when the narrative falls silent, when the crowd’s gaze shifts, and the market is left to its own raw devices. This is where character is revealed, not in the fireworks of an announcement, but in the quiet discipline of the order book and the psychological decay of attention.

I. The Weight of the Niche and the "Narrative Vacuum"

Dusk is engineered for a specific, institutionally-sized problem space: compliant privacy for real-world assets and finance. This is not a retail-friendly meme; it is a long-duration, regulatory-paced endeavor. Consequently, the project exists in a perpetual state of narrative tension. Its most significant potential catalysts regulatory clarity, major institutional onboarding, licensed venue launches operate on timelines measured in quarters or years, not days. This creates extended periods I term the "narrative vacuum."

During these phases, the project lacks a compelling, tradable story for the broader market. The chatter dies down. Social volume flatlines. For a trader accustomed to the dopamine-driven cycle of hype and speculation, these charts look dormant, almost lifeless. This silence, however, is not an absence of activity. It is a different kind of market, one stripped of thematic momentum and driven purely by structural and psychological forces. The price action becomes a slow-motion battle between the project’s inherent design—its tokenomics, its incentive structures, its very technological focus—and the human behaviors of its holders. In this vacuum, boredom is a powerful actor. It systematically weeds out weak hands who require constant narrative stimulation, gradually transferring tokens to those with a longer time horizon or a more structural view. You can see this in the on-chain data: long periods of low volatility and low transaction counts, punctuated not by organic growth, but by sporadic, often external liquidity events that test conviction.

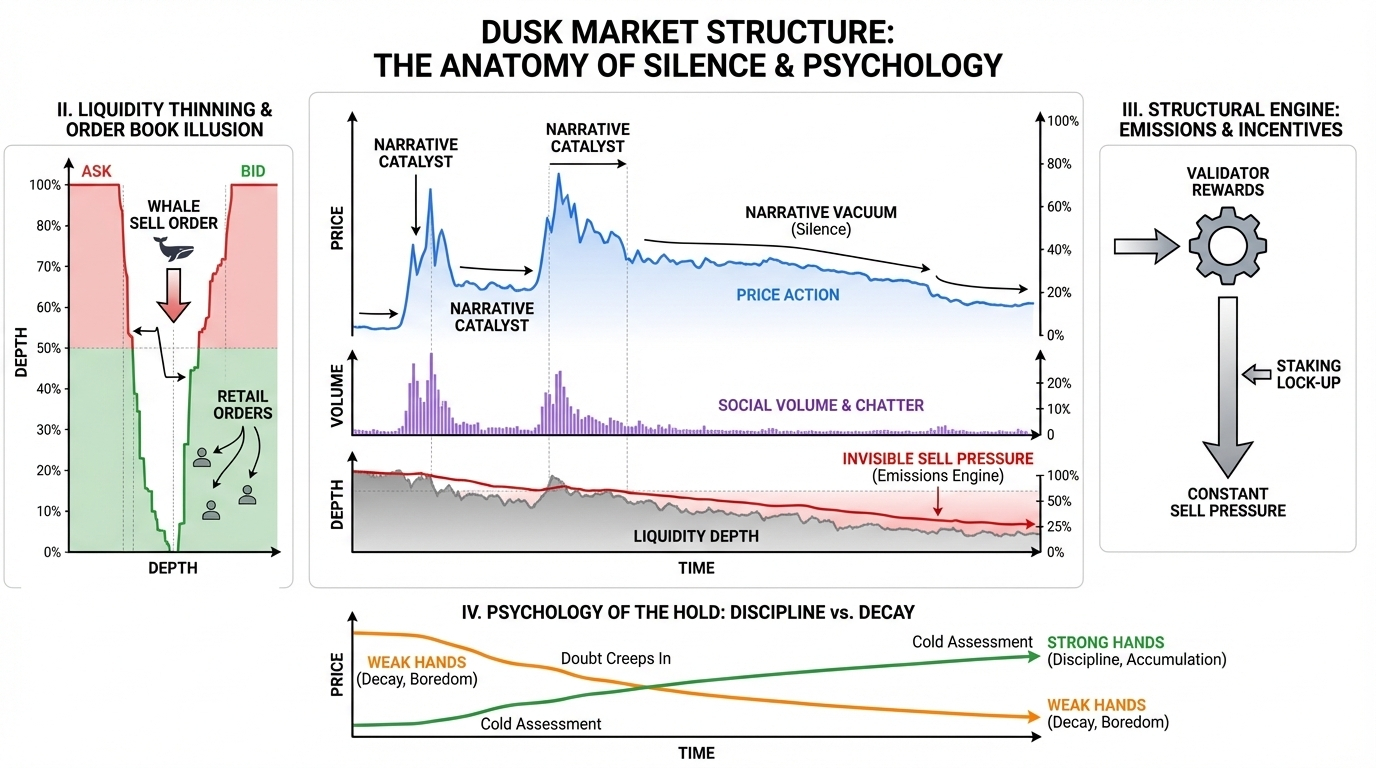

II. Liquidity Thinning and the Illusion of the Book

In the silence, liquidity becomes the supreme landscape feature. For a project of Dusk’s current market cap and exchange distribution, liquidity is perpetually thin. This is not an aberration but a defining condition. The order book on most venues resembles a shallow pool with steep, rocky sides. A modest bid or ask wall can appear monumental, creating false signals of support or resistance. This thinness exaggerates all price movements. A medium-sized market sell order can cascade through several percentage points, not due to a fundamental shift, but simply because it exhausts the available bids. Conversely, a determined buyer can paint the tape green with relative ease.

This environment creates a unique predator-prey dynamic. The "whales" entities holding large, often genesis-era bags sit in profound awareness of this thinness. Their actions, or inactions, dictate the short-term tempo. A decision to slowly drip-sell into available bids creates constant, gentle sell pressure that grinds price down in a way that feels inexorable and sapping to morale. Conversely, their decision to step away and not provide liquidity can lead to a volatile, illiquid drift. The order book, in these periods, is less a transparent record of intent and more a fragile tableau, easily rearranged by a single actor. Trading here requires reading not just the visible orders, but inferring the patience and strategy of those who could place them but choose not to. It is a game of patience and anticipated fatigue.

III. The Structural Engine: Emissions, Incentives, and Invisible Sell Pressure

Beneath the psychological theater of boredom and attention lies a relentless, mechanical engine: the project’s incentive design. Dusk’s Proof-of-Stake security model and its emissions schedule are not merely technical parameters; they are continuous, deterministic forces acting on price.

Validator rewards, paid in newly emitted tokens, represent a constant, programmatic sell pressure. Validators, often operating as businesses with operational costs denominated in fiat or stablecoins, are incentivized to sell a portion of their rewards regularly. This creates a steady, predictable trickle of tokens from the protocol into the market. During high-narrative, high-liquidity periods, this flow can be absorbed by new buying interest. In the silence, it accumulates. It acts as a gravitational weight on price, a force that must be overcome by fresh capital inflow simply for the price to remain stable. One must always account for this invisible faucet, drip-feeding supply into a market where demand is sporadic and narrative-driven.

Furthermore, the "privacy-by-design" ethos, while a core technological value, introduces a unique behavioral friction. For the institutionally curious the purported end-users of the network privacy is a feature. For a segment of the speculative crypto market, it can be a disincentive. The inability to easily track fund flows, whale wallets, or protocol treasury movements in real-time creates an opacity that some capital avoids. This can limit the pool of speculative traders who thrive on chain analytics and copy-trading, potentially leaving the asset to a holder base that is either deeply convicted in the thesis or simply locked in staking contracts. This structural opacity reinforces the liquidity thinness and can lead to moments of extreme mispricing when information finally does break through the privacy barrier, as the market scrambles to price in previously hidden realities.

IV. The Psychology of the Hold: Discipline vs. Decay

This is where the human element confronts the structural and mechanical. Holding an asset through a prolonged narrative vacuum is a psychological gauntlet. The initial thesis "institutional RWA infrastructure with privacy" begins to decay. It is not disproven; it simply loses its emotional and cognitive potency through repetition and lack of confirmation. Doubts creep in: Is the development pace too slow? Is the regulatory window closing? Has the market moved on to a shinier object?

Weak hands are defined by their need for constant validation, for price action that confirms their intelligence. The silence denies them this. They sell not on changed fundamentals, but on eroded conviction, often at the local minima, providing the liquidity for stronger hands to accumulate. The strong hand here is not necessarily a blindly devout "believer," but often a colder, more calculating entity. They may be accumulating based on a valuation model disconnected from short-term narratives, or they may be structural players (validators, ecosystem funds) whose actions are dictated by longer-term operational needs rather than price sentiment. Their buying is methodical, often invisible, and occurs when the market offers tokens at a discount to their internal model, a discount frequently created by the exhaustion of the weak.

Price discipline in such an environment is not about bullish fervor. It is about the quiet assessment of whether the core structural thesis remains intact despite the narrative silence. It is about understanding that the incentive-driven sell pressure is a known quantity, not a surprise. It is about recognizing that the thin liquidity is a condition to be navigated, not a permanent state. The most disciplined actors do not fight the silence; they use it as a filter and a sourcing mechanism. They understand that in a market drunk on noise, the greatest edges are often found in the quietest corners, where assets are priced not on dreams, but on the cold, hard mechanics of their existence and the fraying patience of their holders.

Conclusion

Observing Dusk Network is a masterclass in the dichotomy between long-term technological construction and short-term market mechanics. Its price action during low-narrative periods reveals a market in its purest, most unforgiving form: a shallow pool of liquidity, constantly fed by the mechanical drip of incentive-driven emissions, under pressure from the psychological decay of attention. The project’s very strengths—a niche institutional focus, privacy, a methodical regulatory approach act as brakes on retail hype, ensuring these silent periods are not anomalies but the dominant state.

The conclusion is not a prediction of price, but an observation on behavior. In this environment, narrative is a fleeting catalyst, a gust of wind that moves the price but does not change the underlying currents. Discipline, therefore, performs a specific function when narratives fade. It transforms from a passive act of "holding" into an active process of structural analysis. It means valuing the silence as a source of informational advantage, understanding the order book as a psychological battlefield, and internalizing the relentless math of token emissions. The disciplined participant survives the silence not on hope, but on a clear-eyed assessment of the architecture both of the blockchain and of the market that precariously values it. In the end, for projects like Dusk, the bear market is not just in the price; it is in the wearying, silent space between the stories we tell, and it is in that space where real accumulation and distribution occur, far from the crowd's noisy gaze.