In crypto, liquidity is often talked about as if it were a scoreboard. Numbers go up, screenshots circulate, and total value locked becomes a proxy for success. TVL is easy to understand, easy to compare, and easy to market. Yet beneath that surface, most real financial systems do not run on static pools of capital. They run on credit, flow, and confidence that liquidity will be available when needed.

This is where the difference between appearance and function becomes obvious.

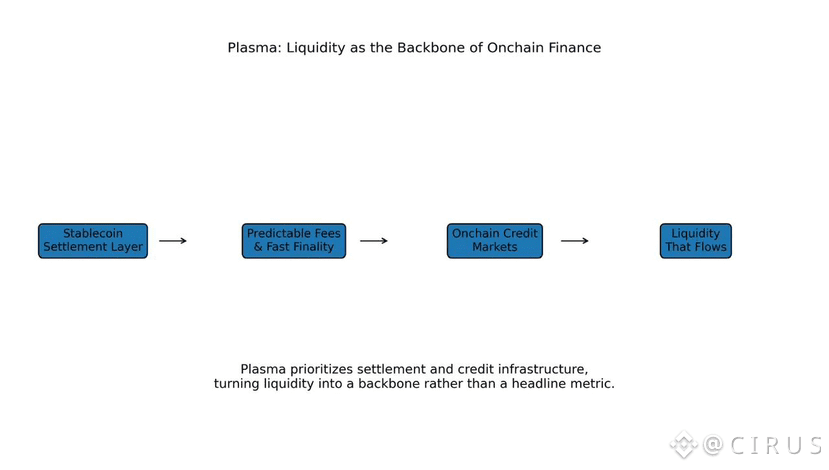

Plasma is built around a more grounded understanding of liquidity. Instead of optimizing for headline TVL, Plasma focuses on something far more important for real-world finance: the ability to move stable value reliably, continuously, and at scale. In that context, onchain credit markets are not a feature at the edge of the system. They are the backbone.

To understand why this matters, it helps to step away from crypto-native metrics and look at how financial systems actually work.

Why TVL Became the Wrong North Star

TVL rose to prominence during DeFi’s early expansion because it captured something real: capital commitment. Locking funds onchain signaled trust in protocols and reduced counterparty risk. For early lending pools and AMMs, TVL was a reasonable shorthand for capacity.

Over time, however, TVL turned into a blunt instrument. Capital parked in pools does not necessarily mean capital that is usable. Idle liquidity inflates numbers without improving throughput. Worse, TVL can be gamed through incentives that attract short-term deposits without creating durable financial activity.

Traditional finance does not measure the health of payment networks or credit systems by how much money is frozen in accounts. It measures them by settlement reliability, liquidity velocity, and the ability to extend credit against predictable cash flows.

Plasma aligns with this latter view.

Liquidity Is a Flow Problem, Not a Stock Problem

At the core of any payment or settlement system is movement. Merchants care about whether funds arrive on time. Market makers care about whether positions can be financed efficiently. Institutions care about whether obligations can be met under stress.

These are flow problems.

Onchain credit markets address this directly. They allow liquidity to circulate rather than sit idle. Capital becomes productive not because it is locked, but because it can be temporarily borrowed, settled, and repaid within predictable parameters.

Plasma is designed as a stablecoin-first settlement chain precisely because stable value is the medium through which these flows make sense. Credit markets denominated in volatile assets introduce risk that overwhelms their usefulness. Credit markets denominated in stablecoins resemble the plumbing of real finance.

Why Settlement Chains Need Native Credit Logic

Most blockchains treat credit as an application-layer concern. Lending protocols are bolted on top of general-purpose chains that were not designed with settlement predictability in mind. This works during calm periods, but it breaks down under load or volatility.

Plasma approaches the problem from the opposite direction. Settlement is the foundation. Stablecoins move with predictable fees, fast finality, and consistent execution. On top of that foundation, credit markets can function without fighting the underlying infrastructure.

This matters because credit depends on timing. Delayed settlement, unpredictable fees, or congestion undermine confidence. Without confidence, credit dries up.

By making settlement boring and reliable, Plasma creates the conditions under which onchain credit can actually scale.

Why Credit Markets Matter More Than Liquidity Hoarding

In real economies, liquidity is rarely fully pre-funded. Companies draw on credit lines. Payment processors front liquidity for merchants. Clearing systems net obligations instead of settling everything in advance.

Onchain systems that rely purely on locked liquidity are inefficient by comparison. They force participants to overcollateralize and pre-position capital, increasing costs and reducing velocity.

Onchain credit markets reduce this friction. They allow participants to access liquidity when needed, repay it quickly, and reuse capital efficiently. This increases effective liquidity without increasing headline TVL.

Plasma’s design recognizes this distinction. It optimizes for usable liquidity, not impressive screenshots.

Stablecoin Settlement as the Credit Substrate

Credit only works when the unit of account is stable. This is why traditional credit markets operate in fiat currencies, not volatile assets. Plasma’s stablecoin-first architecture reflects this reality.

When fees, settlements, and credit obligations are all denominated in stablecoins, risk becomes manageable. Participants can reason about costs and exposures without hedging every interaction. Credit terms become clearer. Defaults become rarer.

This is especially important for merchant adoption, where margins are thin and predictability matters more than yield.

Why Merchants Care About Credit, Not TVL

Merchants do not care how much value is locked in a protocol. They care about whether they can accept payments, issue refunds, handle disputes, and manage cash flow.

Onchain credit markets enable exactly this. Payment processors can front liquidity for instant settlement. Refunds can be issued without waiting for capital to unlock. Chargeback-like workflows can be handled through structured credit rather than blunt reversals.

Plasma’s settlement focus makes these workflows practical. Credit becomes a tool for smoothing operations, not a speculative instrument.

Liquidity Under Stress Reveals the Truth

TVL looks impressive in calm markets. Stress is where real liquidity is tested.

When volatility spikes or demand surges, systems that rely on static pools often seize up. Fees rise, settlement slows, and participants withdraw liquidity to protect themselves. TVL collapses precisely when it is most needed.

Credit-based systems behave differently. As long as settlement remains reliable and counterparties trust the infrastructure, liquidity can continue to flow. Obligations are met through short-term financing rather than liquidation.

Plasma’s architecture is designed for this reality. By prioritizing predictable settlement and stablecoin flows, it supports liquidity even when conditions are less forgiving.

Why Onchain Credit Is Still Early

Despite its importance, onchain credit remains underdeveloped. Much of DeFi still treats credit as a speculative extension of lending rather than as core infrastructure.

This is partly because general-purpose chains make it difficult to build credit systems that behave predictably. Fee volatility, congestion, and reorg risk all complicate credit logic.

Plasma removes many of these obstacles by narrowing its focus. It does not try to be everything to everyone. It tries to be excellent at moving stable value.

That focus is what makes credit viable.

Liquidity as Confidence, Not Capital

At a deeper level, liquidity is psychological. Participants act when they believe liquidity will be there. Credit markets formalize this belief.

Onchain credit markets signal that the system expects flows, not hoarding. They encourage participants to deploy capital productively rather than defensively. This creates a virtuous cycle: confidence increases usage, usage reinforces liquidity, and liquidity supports credit.

TVL, by contrast, often reflects fear. Capital locks up because participants are unsure when they will need it again.

Plasma’s emphasis on credit reflects a more mature understanding of liquidity as confidence rather than accumulation.

Implications for Institutional Adoption

Institutions are accustomed to credit-driven systems. They expect settlement networks to support financing, netting, and predictable cash management. Systems that require full pre-funding feel primitive by comparison.

Plasma’s model aligns more closely with institutional expectations. Stablecoin settlement with native credit logic resembles existing financial infrastructure more than most DeFi designs.

This alignment matters if onchain finance is to move beyond experimentation.

Why TVL Will Fade as a Primary Metric

As onchain systems mature, metrics will change. Just as payment networks are not judged by account balances, settlement chains will not be judged by locked value alone.

Metrics like liquidity velocity, settlement throughput, and credit utilization will become more meaningful. Plasma is built with this future in mind.

By focusing on flows rather than stocks, it positions itself for a phase of Web3 where finance looks less like a game and more like infrastructure.

Closing Reflection

Liquidity is not about how much capital sits still. It is about how reliably value can move.

Onchain credit markets turn liquidity from a static number into a dynamic capability. They allow systems to meet demand without overcapitalization. They support merchants, market makers, and institutions in ways TVL never can.

Plasma understands this distinction. By treating stablecoin settlement as the foundation and credit as the backbone, it moves the conversation away from headlines and toward function.

In the long run, the chains that matter will not be the ones with the biggest numbers on dashboards. They will be the ones where liquidity shows up when it is needed.

That is what Plasma is building toward.