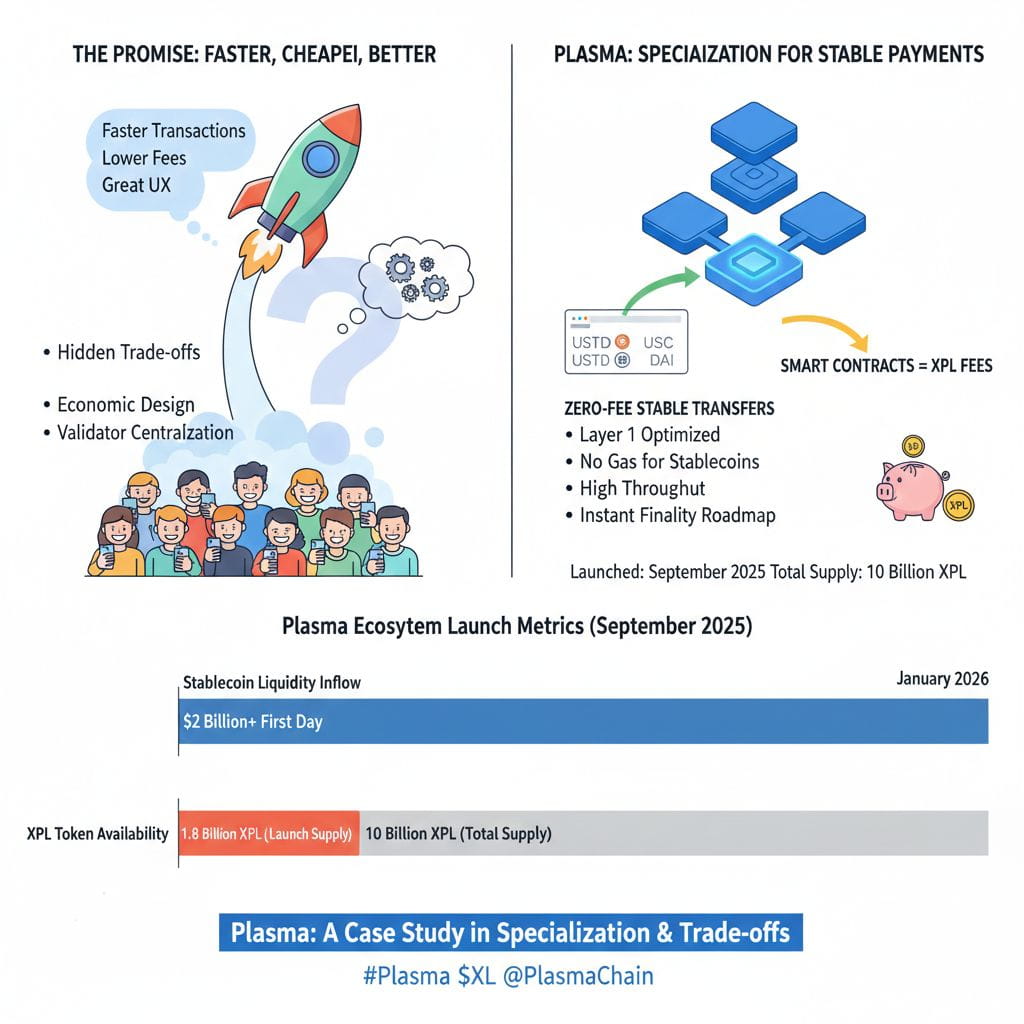

In cryptocurrency, Every halving, another cryptocurrency is created and promises faster transactions, lower fees, and a greater user experience. However, after many moons of buying and breathing through various projects and observation of their development and growth, one thing is certain, there is ever a cost to such gains. In fact, Plasma and its associated token, XPL, are right at the center of this discussion. Launched on mainnet beta last September 2025, Plasma is intended as a dedicated blockchain for making stable payments. Its rapid rise is a perfect case study for these various costs that come with scale and/or speed.

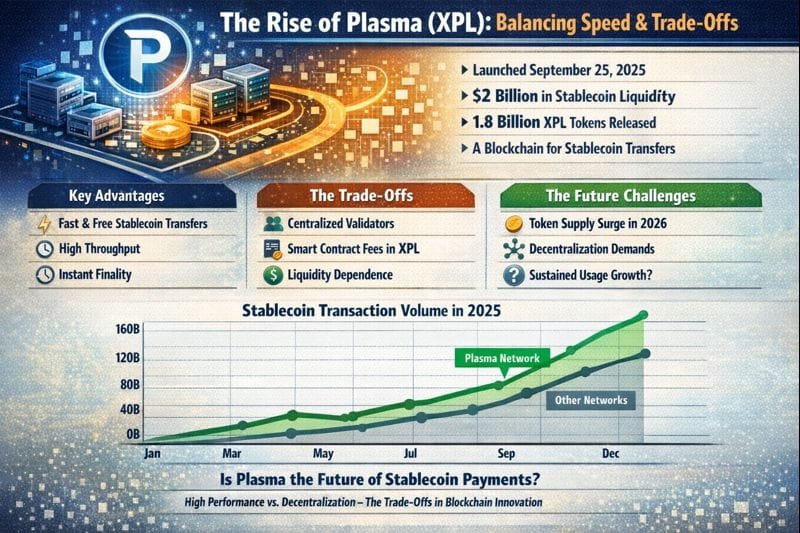

Plasma didn’t emerge without making significant noise. On September 25, 2025, it debuted with over $2 Billion in Stablecoin liquidity being made available across Plasma’s ecosystem of Defi partners, one of the largest first-day inflows of any network in history. Additionally, approximately 1.8 Billion XPL tokens were made available upon network launch, with the total supply being 10 Billion. But for those specifically interested and focused on infrastructure, such an amount and level of interest indicate that there is something to note. Stablecoins aren’t just a sidebar conversation anymore. They’re becoming a standalone conversation.

To make sense of this trend for Plasma, let’s first discuss exactly what Plasma does. Fundamentally speaking, Plasma is a blockchain network with Layer 1 scaling optimized for stable coin transfer. Instead of simple tokenization of stable coins on normal networks, Plasma structures its entire network based on stable coin transfer. Not only is there no gas for simple stable coin transfer, but users do not need to own any native asset in order to transfer stable coins like USDT or USDC.

Such an approach resolves a real problem. Indeed, trillions of dollars in transaction volume were processed globally through stablecoin transactions in 2025, as the supply of stablecoins topped $160 billion. However, a majority of these transactions utilize platforms like Ethereum or Tron, which face major issues like congestion, transaction fees, or throughput. Indeed, Plasma has a strong focus as a layer built around a roadmap that offers a higher throughput, with near instantaneous finality, eventually utilizing Bitcoin as well as cross-platform solutions.

With respect to its design, the bold choice Plasma has made is that of specialization over generalization. This has enabled Plasma to achieve tremendous efficiencies, but here is also the point at which tradeoffs arise. While a general-purpose chain is designed to deliver on decentralization, composability, and neutrality, a specialized chain such as Plasma is designed to deliver on throughput, predictability, and costs.

One technical compromise is with regards to the structure and decentralization of the validators. High-performing networks utilize a healthier whitelist with regards to the validators to ensure the network runs quickly. Plasma has a roadmap to further decentralize the network with regards to the validators by the year 2026. While this is great for reliability in the initial stages, there is need to consider issues surrounding the governance structure within the first stages. While institutions might appreciate the safety of the current structure, the crypto purist will view it as a compromise.

Another important trade-off is economic design, where plasma has free transfers of stablecoins but incurs XPL when executing a smart contract. The former reduces costs but makes token demand focus more on smart contract activity. From a trader's point of view, I find it interesting how it disrupts the dynamic well-known to other systems in which users pay gas costs but now generate value through applications, validators, and infrastructure participants. Moreover, in a practical sense, this also means that XPL's value will depend more heavily upon developers adopting XPL and applications developing, a slower and less predictable process.

Additionally, there is a liquidity-driven growth strategy. Throughout 2025, Plasma has raised a lot of money in the public token sale. The public token sale raised approximately 373 million in donations. Besides that, there were various institutional pre-deposit programs. As a result, there has been a lot of liquidity before officially launching on mainnet. However, there will be supply challenges in the coming years. The major token supply starts in mid-2026. It remains to be seen if realness can sustain itself.

Why is Plasma trending right now? Well, there are a number of different reasons. Timing is perhaps one part of that. Regulatory clarity on stablecoins improved dramatically this year, at least for jurisdictions like the US and Asia. Financial organizations have become increasingly willing to test out on-chain settlement. Plasma launched with existing infrastructure, existing liquidities, and existing works-in-progress. Furthermore, early January 2026 saw a NEAR Intents integration for large volume stablecoin flows across a number of different chains. This is intended to serve the needs of enterprise dollar flows. In other words, Plasma is serious about real-world applications and is not merely another attempt to fuel further DeFi speculation.

From a personal standpoint, I would argue that in a larger sense, plasma represents a change in cryptocurrency as a whole, as people in this market, along with others in crypto as a whole, begin to transition from narratives of pure, unadulterated decentralization and instead look more towards systems that effectively facilitate transfer of resources. While this isn’t a dismissal of ideologies, pragmatism is nevertheless ascending.

Nevertheless, a certain level of compromise cannot be avoided. For a high-performance blockchain system, some level of decentralization, composability, and even neutrality will almost definitely be sacrificed. However, would it be worthwhile if we consider stablecoin payments wherein a user demands high-performance guarantees, zero costs, and instantaneous confirmation?

Plasma now has to demonstrate that real-world transactional volume can increase faster than token supplies are released. If they can achieve this, they will be showing what a new class of financial infrastructure looks like blockchains that feel less like experimental platforms and more like digital payment rails. If they cannot achieve this, they will be joining other case studies in just how difficult it can be to balance speed, scale, and decentralization.

Either way, Plasma represents perhaps the most obvious real-world case for the trade-offs in the development of a high-performance blockchain. And for those interested in the movement of infrastructural trends rather than the immediate price action itself, it is certainly worth paying close attention to.