$BTC MicroStrategy: A 'Dangerous Game' Betting the Company's Fate on Bitcoin

Recently, MicroStrategy has been trending, with many predicting it to be the biggest risk. MicroStrategy holds 710,000 bitcoins. You may have heard of people mortgaging their houses to invest in stocks, but have you ever imagined a publicly traded company betting its entire fate on a digital asset—Bitcoin? This is not a movie plot; it is a real business story unfolding before our eyes. The protagonist is an American company called 'MicroStrategy,' which is conducting the boldest and most dangerous experiment in business history.

The transformation from software company to "Bitcoin whale."

MicroStrategy was originally a serious publicly traded software company, developing business intelligence tools and living a relatively stable life. But in 2020, the company made a shocking decision: to announce it would use company funds to buy Bitcoin, claiming it was to "hedge against dollar depreciation." Initially, they invested $250 million. If the story ended here, it would just be a somewhat aggressive investment decision.

However, the real turning point is that they tasted the sweetness. When Bitcoin prices rise, the value of the Bitcoins held by MicroStrategy skyrockets, and the company's market value rises accordingly. Thus, a bold idea was born: since the market recognizes our holding of Bitcoin, why not buy more?

Where does the money come from? MicroStrategy demonstrated astonishing "financial tricks": first buying with company cash, then issuing bonds to borrow money, and when the borrowed money runs out, issuing more company stock to continue buying. It's like a collector who, having gotten a taste, can't help but acquire their desired art piece, even if it means borrowing money.

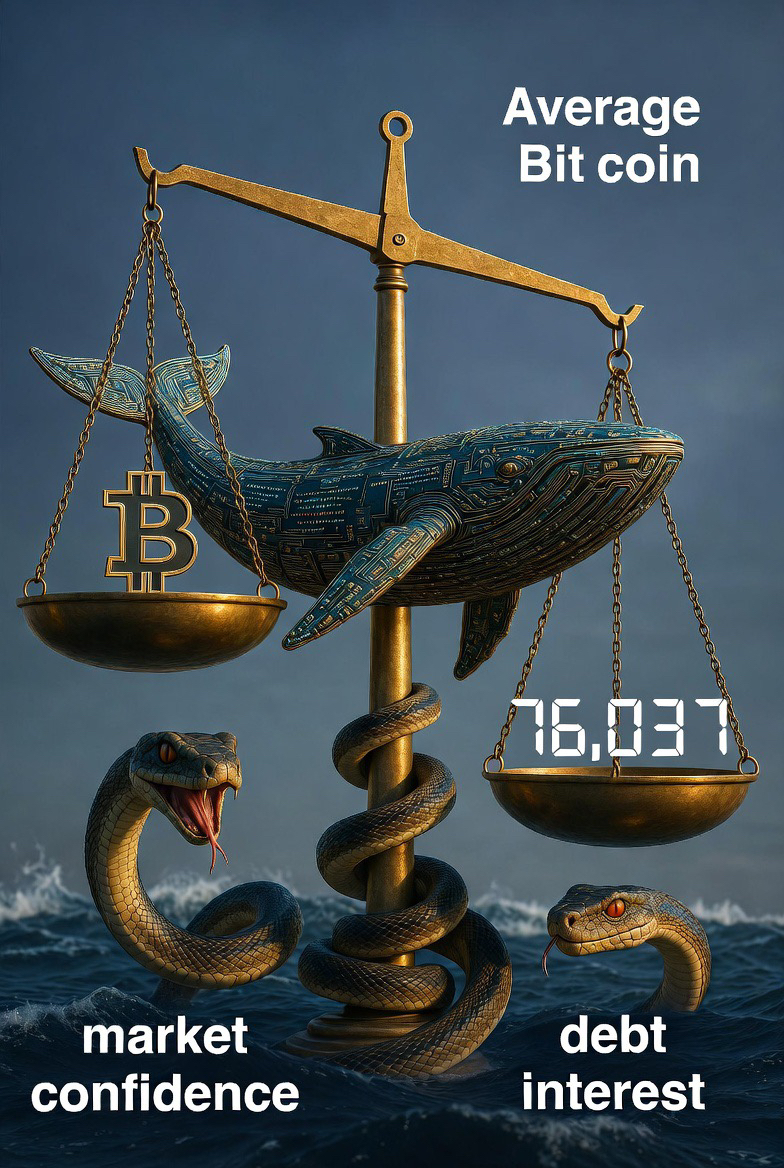

Now, MicroStrategy holds more than 710,000 Bitcoins, equivalent to 3.39% of the total Bitcoin supply worldwide. If we imagine these Bitcoins as gold, then MicroStrategy is like sitting on a mountain of gold. But the problem is that the cost of acquiring this "mountain of gold" is not low—an average purchase price of $76,000 per Bitcoin. Currently, Bitcoin's market price is hovering near this cost line, like a Damocles sword hanging over their heads.

"\u003cc-16/\u003e

The core logic of MicroStrategy is built on a delicate but fragile foundation. Imagine you have a jar of gold coins, and then you tell everyone: "Look, I have this much gold!" If everyone believes your gold is valuable, and is even willing to pay a higher price than the gold itself to buy shares in your company, what will happen?

At this point, you can do something magical: issue more company stock, using the money from selling stocks to buy more gold. And because the proportion of stock issuance is controlled properly, the original shareholders' "gold share" not only does not decrease but actually increases. It's like magic, creating more assets out of thin air.

Once this model starts to operate, it forms a seemingly perfect "flywheel":

1. Bitcoin price rises → Company assets appreciate.

2. The market is optimistic about the company → Stock price rises (and the increase exceeds Bitcoin itself)

3. Stock prices are high → The company can issue more stock to get more money.

4. Exchange for more money → Buy more Bitcoin.

5. Bitcoin holdings increase → Market is more optimistic about the company → Stock price continues to rise.

This cyclical process forms a self-reinforcing myth of growth. The stock price of MicroStrategy has become one of Wall Street's brightest stars in recent years, largely due to this "flywheel" in motion.

But all "perpetual motion machines" have a stopping point. This flywheel has a fatal flaw: the company's stock price must always be higher than the actual value of the Bitcoins it holds. This premium is like the "fuel" that keeps the flywheel spinning. Once the fuel runs out, the flywheel will slowly come to a stop, or even reverse.

The balancing act at the critical point.

Currently, MicroStrategy is standing at a delicate critical point. Bitcoin's price is fluctuating near the cost line of $76,000, which means the company's massive Bitcoin assets are facing the risk of turning "floating gains" into "floating losses."

Imagine that you borrowed money to buy a house, and the house price just fell to the price you bought. Although you haven't really lost yet, the monthly mortgage interest is a real expense, the bank may start to get nervous, and neighbors may start gossiping. MicroStrategy is now in this situation.

To maintain confidence, MicroStrategy adopted a dual approach:

On one hand, they continue to buy Bitcoin, using real money to declare to the market: "We still have confidence!" On the other hand, they need to find ways to maintain the stock price and ensure that critical "premium" does not disappear.

Fortunately, MicroStrategy is not unprepared. They hold several important "trump cards":

First, there is an ambitious "42/42 plan": planning to raise $42 billion by issuing stocks and another $42 billion by issuing bonds between 2025 and 2027, totaling $84 billion—all for purchasing Bitcoin. This amounts to announcing: "Our Bitcoin acquisition plan has just begun!"

Secondly, they prepared a cash reserve of $1.44 billion. This money is not used to buy Bitcoin, but is the company's "safety cushion", specifically for paying debt interest and various expenses over the next 21 months. This means that for a considerable period, the company does not need to sell any Bitcoins to operate normally, avoiding the dilemma of being forced to sell at low prices.

The lurking "death spiral": when the first domino falls.

All sophisticated financial designs fear one situation: the collapse of trust. For MicroStrategy, the most terrifying nightmare is not the short-term volatility of Bitcoin prices, but the beginning of the "death spiral."

How does this spiral start? Imagine a scenario like this:

One day, for some reason (perhaps due to the pressure of debt maturity or a sudden cash flow need), MicroStrategy sold a small portion of its Bitcoins, for example, a few thousand. This is just a drop in the bucket compared to the total holding of 710,000.

But the market's reaction will be entirely different. Investors will immediately become alert: "The largest Bitcoin holder has started selling! Why sell? Are they struggling? Will there be more sell-offs?"

Panic begins to spread. Retail investors may think: "If even the largest holder is selling, should I run first?" So they rush to sell their Bitcoins or MicroStrategy stocks. Selling leads to price drops, price drops trigger more selling—a typical stampede event.

More critically, MicroStrategy's stock price is likely to plummet due to this panic, causing the "premium" between the stock price and its Bitcoin net value to disappear. Once the premium disappears, the "flywheel" that relies on it will cease to operate. The company can no longer obtain cheap funds through stock issuance, and may instead face issues such as insufficient collateral and declining financing capacity due to falling stock prices.

If Bitcoin prices fall simultaneously, the company's assets will shrink, the balance sheet will deteriorate, and creditors may demand early repayment or additional collateral. To cope with these pressures, the company may be forced to sell more Bitcoins, exacerbating the price decline... thus forming a downward spiral, with each link accelerating the deterioration of the next.

Michael Saylor, the founder and CEO of MicroStrategy, has repeatedly stated that their strategy is to "hold Bitcoin forever" and never sell it. This is not just a belief in investment, but a necessity to maintain this fragile balance. Because even selling a little bit could trigger the market's most sensitive nerves.

Great gambler or a madman at the end of the road?

Today, MicroStrategy is no longer just a "Bitcoin-holding company"; it has become a key node in the Bitcoin ecosystem, a signal amplifier, and a thermometer for market confidence.

Supporters view Saylor as a visionary, believing he boldly "Bitcoinized" the company's balance sheet and is a pioneer of financial innovation. In the eyes of his fans, MicroStrategy is not merely a software company, but a "Bitcoin holding company" and the best vehicle for ordinary people to invest indirectly in Bitcoin through the stock market.

Skeptics view this experiment as a dangerous Ponzi scheme, believing that MicroStrategy has built a house of cards with leverage and capital games. Once the cryptocurrency enters a bear market, this building may collapse in an instant, leaving a mess behind.

This is essentially an extreme test of belief. It tests whether the market truly believes in Bitcoin's long-term value, whether a public company can completely reshape itself through a non-traditional asset, and tests the modern financial system's tolerance for such radical experiments.

The outcome of this gamble is yet to be revealed. MicroStrategy may become a classic case in future financial textbooks—perhaps a model of successful transformation or a warning of the destruction caused by over-leveraging. But regardless, it has provided us with an excellent observation window: what happens when a company deeply ties its fate to a highly volatile digital asset?

Every time Bitcoin's price touches $76,000, the entire cryptocurrency market holds its breath. This number is not just a line on a technical chart, but a lifeline for a company's business model, a critical point for a financial experiment.

In this digital jungle composed of code, belief, and capital, MicroStrategy may be the ultimate hunter, or it may become the most spectacular prey. And in this grand play, each of us is not just an audience; to some extent, we are also participants in the crowd—because its ending will profoundly affect our understanding of assets, value, and the boundaries of companies.\u003cc-32/\u003e\u003ct-33/\u003e